Jump to “How does it work?” here

A Quality Education

TASK is The Academic Civic Science Challenge (tacsc). TASK rates academic universities and institutions by National Advance

This assures that their curricula are creating experts, leaders, and successful societies

The Annual Universities TASK Report ranks universities from highest to lowest by their record of teaching quantitative highest-probability-of-success science and approach (epistemology)

TASK showcases Universities that govern all faculties with a Civic Science Program and Standard of Research (see CS-BOK). Civics faculties include Economics, Business, Finance, Law, Government, Education, and Social Science, but most engineering and natural science faculties mandate Civics electives as well

Transparency

Source statistics for all TEPs are available online so anyone can confirm or build charts for the same results. All Data here must be properly cited and summarized credibly by Edgar Alan Poe’s famous truism (with my Dad’s twist):

Believe nothing you hear, half of what you read, and everything you see

Read how TE ensures essential Human Rights, incomes, and national production and prosperity is maintained in Hybrid Economies on csq1.org/Transition-Economics

How does a Hard Science in evidence-based Civics Work?

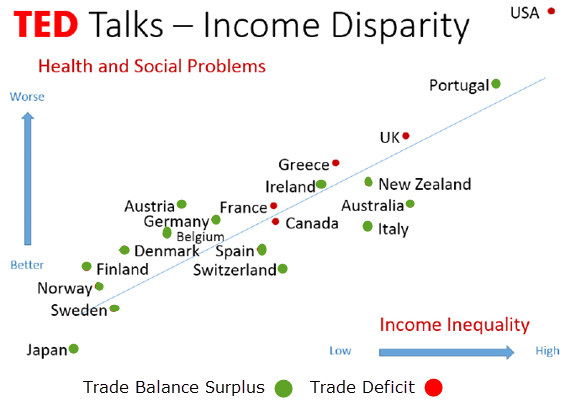

Let’s begin by looking at a report by Professor Richard Wilkinson’s Nottingham University Research Team TED Report on Financial Inequality and Social Problems in 2013. See his TED Talk here …

13 Social Problems in 20 countries are higher with inequity

Nottingham’s report is compelling because it shows conclusively that 13 social problems are caused by financial inequality in 20 surveyed countries.

One sanity check for any civic science, therefore, is that it must confirm financial inequality and social problems have a similar relationship. Both in the countries proven by the Wilkenson Report, and in every other country too.

To prove that the statement: “Financial Inequality causes (is causal to) Social Problems” is a true statement in every nation, we have to confirm it in 220 countries, in high/medium/low-income nation comparisons, in democracies/monarchies, Latin/Asian/Pacific/African Regions, and so on.

Surveys of 13 social problems in 18 countries might sound like enough evidence to convince anyone, but what other information is available to bolster this report’s claim of “Causality in ANY society”? Which other measures can confirm that financial inequality reliably creates social problems – and that correcting the problem improves economies too?

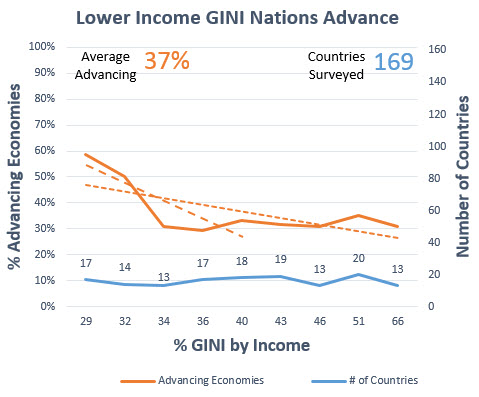

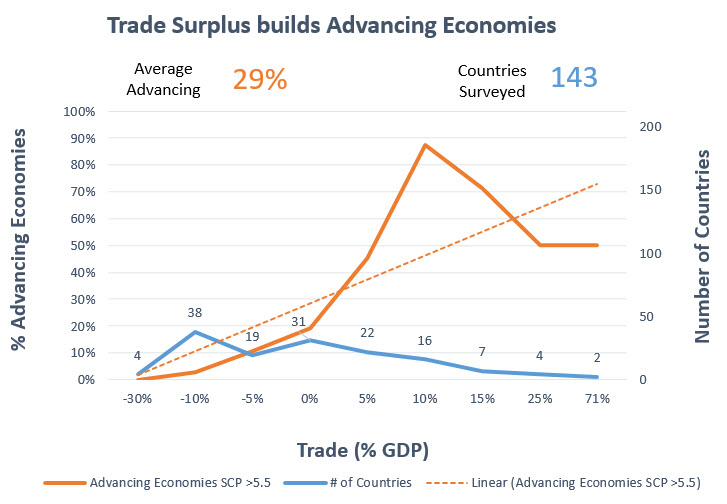

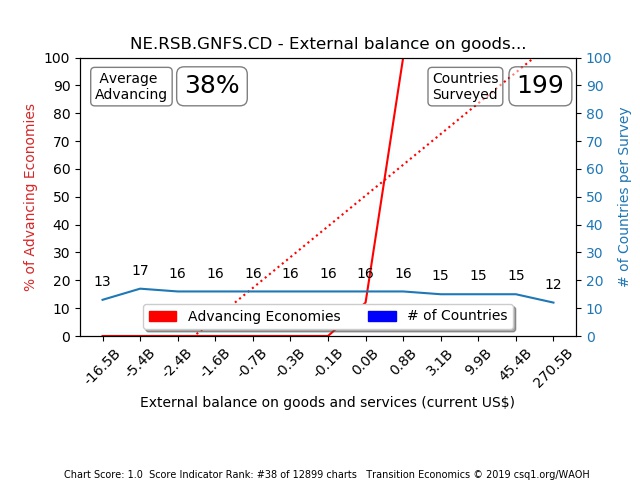

As luck would have it, there seems to also be a similar correlation to social problems when we look at “Trade Balance” – of all things. We can see in the chart below that the nations in the Nottingham survey with trade surpluses, also exhibited low social problems and lower inequality.

Trade Surplus nations (with a positive Trade Balance = Export – Import) are grouped to the left of the chart, while Trade Deficit nations are grouped to the right – as seen in Income Inequality nations

Trade Balance is higher in high Social Contract Nations

Why are Trade Balance AND Financial Inequality valid determiners of Social Problems?

Why are Trade Balance AND Financial Inequality valid determiners of Social Problems?

A lot is going on in an economy, and here we see that both a social measure and an economic measure appear causal to social problems (able to cause or correct them). Why? Perhaps it’s because higher financial equality in a nation permits more citizens to increase opportunities and to contribute to start-up businesses, which generates trade revenues from this increase in local production.

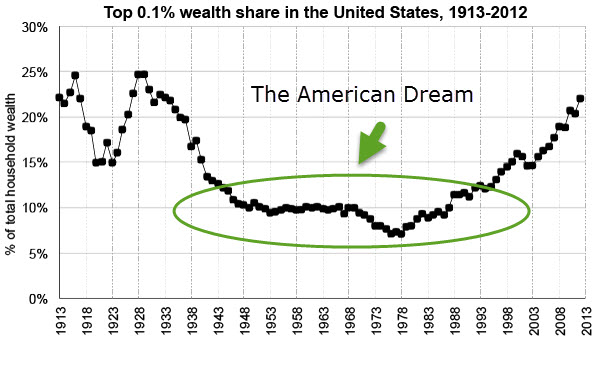

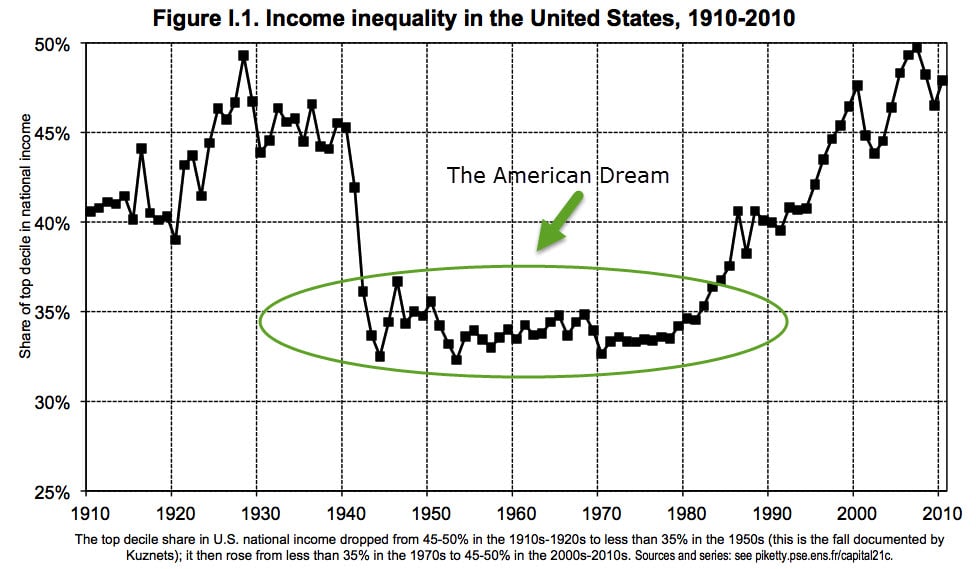

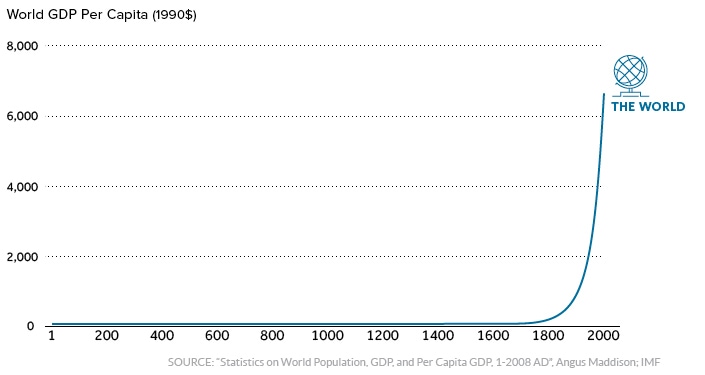

And, we can also learn from history. Today is a time of mature capitalism, imbalance, populism, clear misleadership, and collapse but things were not always this way. What did Financial Inequality (and Trade Balance) look like during the greatest boom economies of all time – just 70 years ago?

The United States, under the direction of Franklin Delano Roosevelt and then Harry Truman, created the greatest economy in history. Let’s take a closer look at that success.

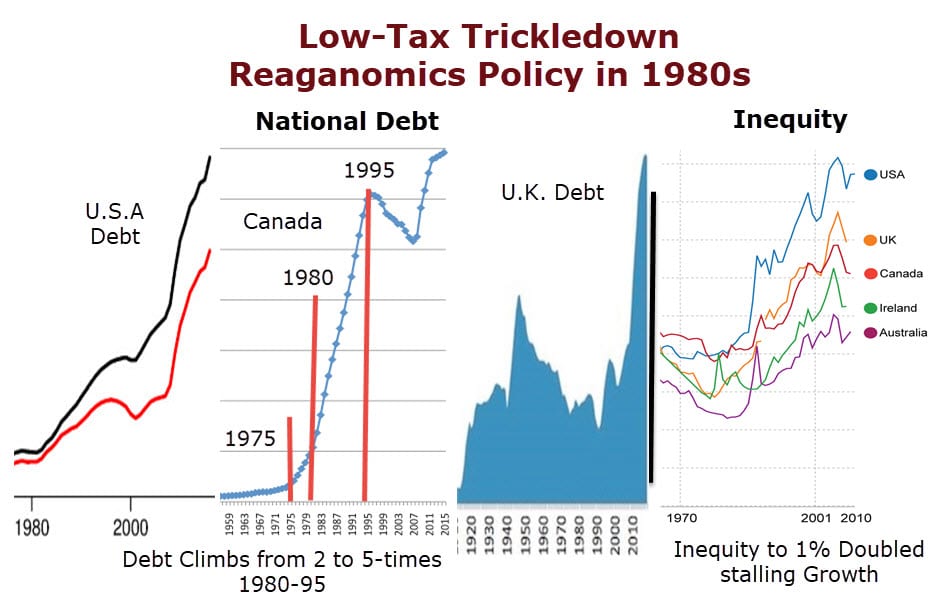

We can see in the charts above, that financial inequality was much lower during the economic boom that began in the late 1930s. That economic boom can easily be said to have been caused by the correction of the inequality created during the 1920s and the Great Depression (another Mature Capitalism and period of imbalance – like today). Wealth Inequality almost doubled between 1923 to 1928 and it stayed high until 1940’s dramatic correction.

Can you also notice that Trade Balance changed as Inequality soared again in the 1980s?

What built that boom economy? Can you tell?

- Did WAR explain the boom economy of the 1950s and 60s? NO. World War I did not create a boom economy afterward; rather, it created the Great Depression. The US has been at war for the last 100 years and its production is collapsing for the last 40 years consistently

- Did GOVERNMENT SPENDING create the boom economy? NO. Government Spending is unchanged or higher as the US collapsed for 40 years

- Did FINANCIAL EQUALITY create the boom economy? YES. Based on everything we see above, this is the truthful answer

So, the chicken-and-egg question of “Does money in the hands of many citizens create a strong economy?” has an answer. Yes.

Does putting money in the hands of a few wealthy oligarchs create a strong economy – as things are today and in the 1920s (per Wealth Theory, Trickledown, and Transition Economy)? No.

This question is answered above – by evidence – and without Transition Economics.

A Context-Driven Approach

When you don’t know what to stand for, you fall for anything

Important to any presentation of statistical information – is Context. Presentations must compare you to successful nations only, they must use recent accurate data, and they must present only credible measures. A credible measure is a measure that is proven highly causal to creating an advancing economy (see “TEP Scores” below). Context in history is relevant also; Debt was forgiven for most European countries in the 1930s from 25% to 250% of their GDP  For example:

For example:

Q1: Is a 3% Salary increase good, bad, or normal? No, it’s bad. A 3% Salary increase is embarrassing in fact.

Why? Since the 1980s, individual and household salaries haven’t budged. It would take a 100% increase in Salaries today, just to come back into balance with where salary levels were in the 1970s.

Q2: Are stock market ups and downs meaningful? No.

Q3: Are GDP lifts important? No.

See Credible Measures explained in the Proofs of the World at our Hands Report

![]()

Confirming Causality with Transition Economics

After researching Trade Balance, we could move next to look for causality in “Household Savings”, or randomly to any one of the over 1,500 other indicators (measures) which every country already collects annually. But, a “guesswork method” is labour-intensive, imprecise, and often unrepeatable. In short, it’s unscientific.

Doctor Wilkenson’s survey and team couldn’t look at all countries, as he wanted to, because of the high workload mandated by their manual survey approach.

So, is there a way to confirm which indicators are the most causal measures from the 1,500 measures that we already collect annually from 220 countries? Can we confirm which already available indicators can influence the collapse and advance of any nation – like Professor Wilkenson’s “Financial Inequality” reports clearly can?

Yes. These are the questions answered, and the problems solved, by Transition Economics (TE) every day.

Finding the same conclusions using TE

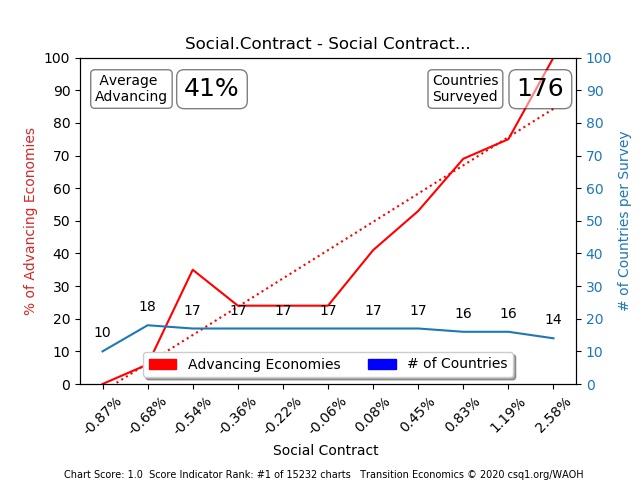

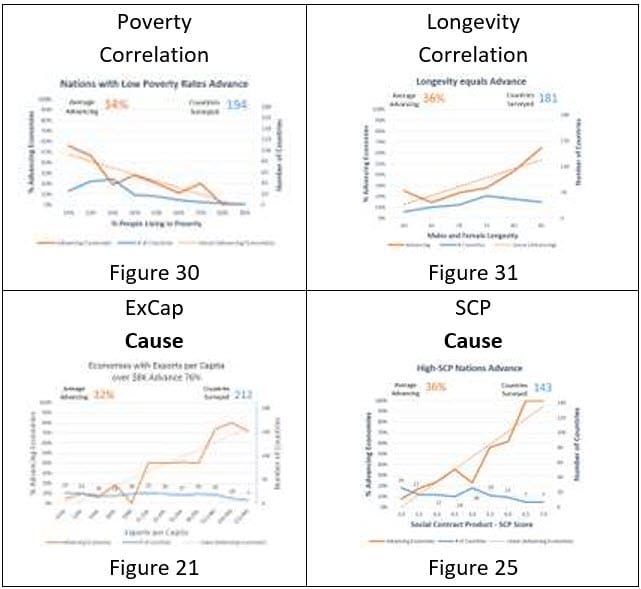

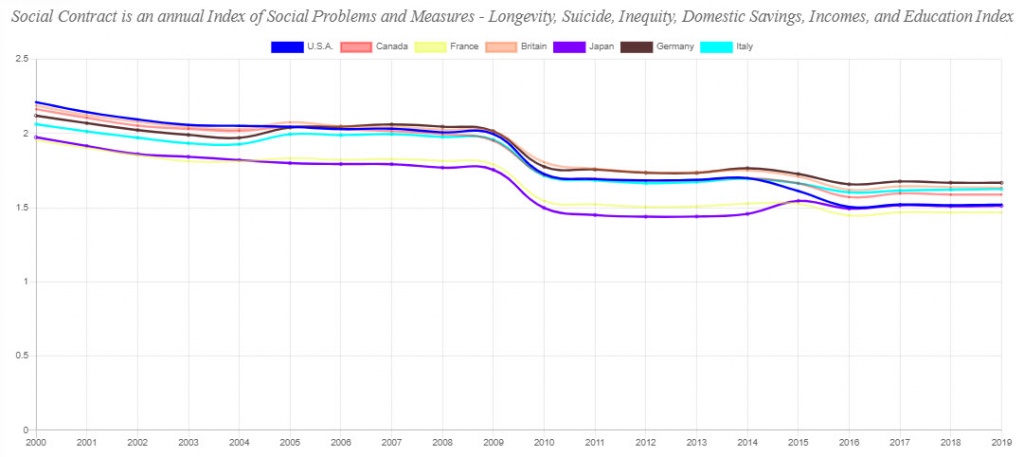

The Nottingham study above is explained by Transition Economics with the “Social Contract” report. Social Contract is an index of social indicators already collected in 180 countries at present. TE builds the frequency distribution chart (TE Proof or TEP Chart) on the right, based on their research, surveys, and data.

How does the Nottingham “Social Problems Chart” look using Transition Economics’ causal Social Contract measures?

Based on the Social Contract’s 179 country survey, the distribution of advancing and collapsing nations group together – from the chart’s left-most advancing nations to its right-most collapsing nations – identical to the distribution of Nottingham’s National Social Problem findings report. You can see from a (simple) Threshold Report below, that Canada and France’s collapse signals were a judgment call as in 2019 they were both marginally collapsing and just barely reaching the status of Advancing. Note that Nottingham’s report presented 2012 social stats.

Legend: Advance/Collapse = original assessment, Trade = Advance or Collapse based on Trade Balance, SC = Social Contract 2019, SC20 = SC 2020, SCP = Social Contract Product (Index), Value = Indicator value, Pop = Population, PRnk is the rank of the country by population size, % is Advance (shown when within 25% of just passing threshold)

– Important Learning –

ANY Causal mix of Social Indicators (indexes whose frequency distribution amplitudes equal 1.0) will show this chart very similarly. We ran the same report for the following Social Contract report as a validation (using MEMS), and I could have run a dozen similar Social Contract indexes the same.

Why build more than one Social Contract Index? Because we have statistics back to 1970 for 179 countries with the first list of three indicators above, but – we only have statistics to the year 2000 for 180 countries that reported the six indicators in the second report.

Indexes with more indicators are best, but data is not always available to support our need for historic trend and context validation. When a report shows Social Contracts have improved in nations where conditions diminished, that report is still useful for noting events, peaks, and valleys in time – but cannot be a truthful Causal report.

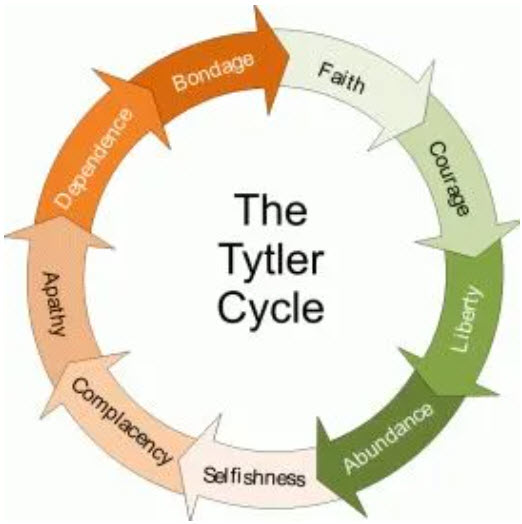

Note: Countries further along a Tytler Cycle, that have grown prosperous and lazy without responsible Civics training, are vulnerable to falling prey to an Ideology War easily. Whereas nations that have been through real wars and real adversity, recognize the importance of nationalism and human rights, and quickly reject Open Borders and Anti-family values or depopulation indoctrinations. Canada or Western Europe versus Croatia or Russia – are examples of this point.

Note: Countries further along a Tytler Cycle, that have grown prosperous and lazy without responsible Civics training, are vulnerable to falling prey to an Ideology War easily. Whereas nations that have been through real wars and real adversity, recognize the importance of nationalism and human rights, and quickly reject Open Borders and Anti-family values or depopulation indoctrinations. Canada or Western Europe versus Croatia or Russia – are examples of this point.

Canada puts their citizens in homeless camps while protecting Globalist Open Borders policies, puts tampons in public men’s washrooms, and suspends its students for not calling males female; while Italy, Croatia, or Russia reject obvious indoctrination and insanely foolish sheep-like followers.

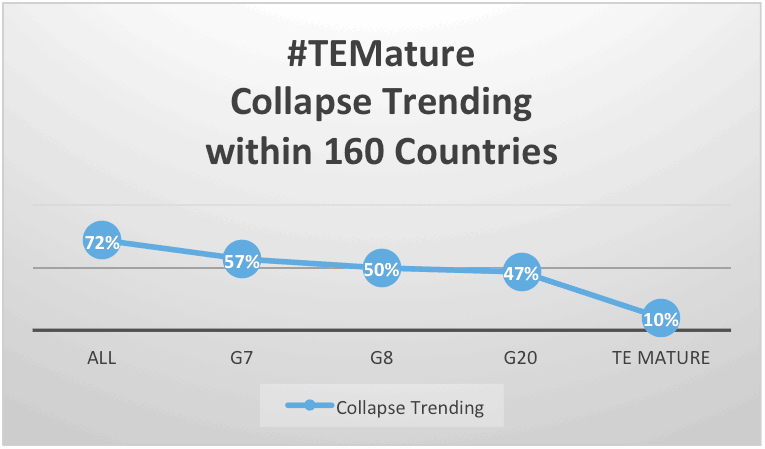

90% of (48 of 54) large democracies are collapsing in the West, while citizens battle DEI laws in the workplace and approach World War III. And still, we can’t vote for Advance – because its not on our ballot cards.

These are the devastating, easily corrected Social Problems that hinder Human Advance – that TE corrects.

Important Measures & Causality are measurable

with TEP Scores and Context Validation

We know that the Transition Economics Advance and Collapse survey results are accurate because we validated the Social Contract measure to have a TEP Score equal to 1.0, and we were also able to run through a Context Validation Process with the Wilkinson Report and the other supporting historical charts above.

Click here – to read our Science of 70% tutorial on how to recreate any TEP chart for yourself

Click here – to view the indicators that make up the Social Contract Index

Click here – to read an advanced explanation of how to read TEP Charts

Click here – to view 945 other sortable and filterable Indicator TEP Scores

Click here – to view the WAOH Library’s Data Science webpage, for many more TEP Scores, Indicators, and Indexes

Click here – to sign up for Civic Scientist training and certifications, so that you, and your teams, can become experts of Civic Science too

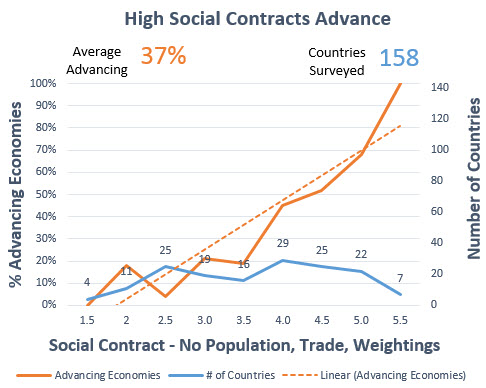

The Social Contract Index TEP Chart

A Causal TEP chart like Social Contract (SC), explains that countries with low scores collapse reliably – 100%, while countries with a strong score advance reliably – 100%.

We call Social Contract “Causal”, or a “Causal Indicator” because its TEP Score is a perfect 1.0. A TEP Chart’s “Score” subtracts the highest frequency distribution (FD) Y-value (for SC it is 100%) minus the lowest Y-axis value – 0%. 1.0 – 0 = 1 .0.

We call Social Contract “Causal”, or a “Causal Indicator” because its TEP Score is a perfect 1.0. A TEP Chart’s “Score” subtracts the highest frequency distribution (FD) Y-value (for SC it is 100%) minus the lowest Y-axis value – 0%. 1.0 – 0 = 1 .0.

TEP Scores are frequency distribution amplitudes.

A score of 1.0 indicates the highest possible causality score – as confirmed by the reporting of 176 countries (in this Social Contract report).

We can also rank TEP Charts that share a score of 1.0, by counting the total number (or %) of advancing nations in their highest value range.

Now, we have a numeric approach to finding both causality – and causal measures, like Wilkenson’s Social Problems above.

So, we no longer have to rely on Classic Economics’ hit-and-miss guesswork, logic, theory, consensus opinions, modeling, or mathematic projection.

Adding more measures and collections

Can we add measures, to those measures that are already currently collected by every nation today? Yes, of course.

Professor Wilkenson’s team struggled to collect obesity, suicide, and other stats in just 20 nations. When these stats collections are budgeted, staffed, reported country-by-country, and then consolidated for 220 countries, perhaps also by income and wealth quintile, then TE’s TEP Reports can zero in on problems and solutions very reliably.

Every problem is solvable, and the first step to solving a problem is finding out that you have one. Everything measured can usually be improved.

TE allows us to drive economies to success consistently

With a numeric approach, we can automate the computation work; we can use Machine Learning techniques to quickly find and compare every variation and combination, of indicators and indexes that yield TEP scores of 1.0 – using Social measures, Economic measures, or a combination of both. We have used this approach to discover TEP Reports that are so causal that they group 38 (of 200) Advancing countries at their highest frequency distribution range.

A Social Measure is either an individual indicator or an index of measures, that is composed of social measures entirely – like Longevity, Education, Infant Mortality, or Social Contract

Economic Measures – are indicators or indexes composed of economic measures like Trade, GDP, Government Spending, and similar.

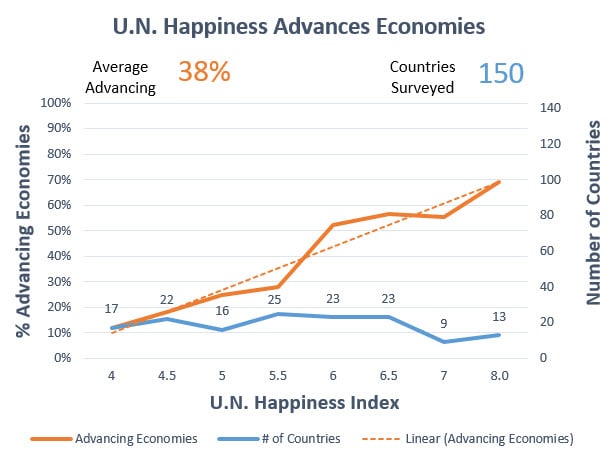

Socioeconomic Measures – are mixed measures which are a combination of the two – Social Contract Product and the United Nations’ Happiness Index – are two examples of this

Basic Principles: Economies are High Transaction Systems

Trillions of daily transactions means that “highest-probability-of-advance” policies WILL build advance reliably in any economy, and the same is also true in reverse – “highest-probability of collapse” policies will collapse economies reliably.

Advance Policies – explain FDR’s Greatest Economy in History – and …

Collapse Policies – explain the GOP’s Neoliberalism Wealth Theory policies of the 1920s, which created the Great Depression in just a handful of years

Adoption Delay

What barriers stop the adoption of a simple, transparent, scientific approach that builds strong economies reliably?

Many of us don’t realize that it took Einstein’s 1905 Theory of Relativity, 20 years to be accepted in the West.

Adoption, the normal resistance to even essential change, is the elephant in any room that will slow TE’s acceptance similarly. Human nature explains that our vaulted Professors, awarded Nobel Laureates, Experts, and Academies have all written textbooks, authored articles, lectured, and peer-reviewed one another – and all of their labour has been based on easily proven-failed theory.

A job title makes no one an expert, and the Swedish Central Bank’s Nobel Prize for Economics has awarded only unscientific theory ever since its inception in 1968. Fictions have vaulted non-experts – and therefore non-leaders, into high positions as economic leads, and these people have been asked to create important policies and programs based on their mastery of a proven failed theory (fiction). This is a serious miss, for academics and peer-review processes, that is going to require some hard introspection, explanation, and KPI-driven performance management to correct

As individuals, it’s not our fault that we didn’t learn responsible civics. Civics takes training, and in the past, we didn’t have access to data from 220 countries as we do today.

Bloodletting and lobotomies were the highest forms of pseudo-science not so many years ago, and then those practices were discounted in a never-ending cycle of new learning – and adoption.

A simple new science like TE proves that leadership, education, and approach/processes have been sub-standard and harmful; bruising egos and besmirching the reputations of high-IQ, well-intended, and previously-esteemed researchers and teachers.

In hyper-competitive mature capitalisms, there are compelling personal and professional reasons for whole faculties to reject, discount, or adopt a new science only by their explanations and terms.

TE is a big challenge for existing social faculties because it is a computer science, which means faculties presently filled with thousands of math professors, are unqualified to teach and supervise TE.

Given unlimited time, economics teachers will: learn computer science, update their skills and research, and assimilate this new science while minimizing any professional embarrassment.

The problem with allowing adoption to take a normal course today is that TE is important. Transition Economics is needed immediately – to save lives, stop wars, and correct collapse. Universities, therefore, must minimize normal adoption delays so that a scientific approach can lift today’s dangerous social and economic collapses as quickly as possible.

Civic Science is exceedingly simple:

When you Fund Advance Policies and Don’t fund Collapse Policies, you are mathematically guaranteed to build a successful economy and society

A professional engineering office would re-phrase this to say: When you professionally Change Manage and Performance Manage your country (region by region) to improve your Advance Policy measures, then your Economic Advance is Guaranteed

“Collapse” is expensive and dangerous, so the performance management of causal indicators is essential to the responsible leadership of any nation. In any democracy, therefore, you only want to vote for Political Teams that implement Advance Policy – and who are also (preferably) endorsed, certified, and monitored by CSQ Research Certification programs.

In Summary:

- By improving your Social Contract score, you WILL advance your country

- If you do nothing, things will remain collapsing or advancing at current rates; and,

- If you drop your score you will collapse ANY country – no matter how strong it is

Here at CSQ Research, this is how we teach economic researchers and Civic Scientists to Double Your Economy and to build World Peace reliably.

Civic Science’s Knowledgebase

The hunt for causal reports never stops.

The World Inequality Database (WID) has been working on an indicator for wealth inequality for years.

The Palma Index (10% highest incomes divided by 40% lowest incomes) appears promisingly causal but inconclusive with just 44 countries in their surveys to date.

We have very recently found a causal report for Adult Wealth Inequality – in Credit Suisse’s Mean Wealth per Adult ($US) Report. This means that “Wealth per Adult” can be counted among the other important measures of collapse or advance for any country. Note, however, that the “sweet spot” in some Adult Wealth TEPs shows that causality decreases (drops to 70% from 100% advance) for the 13 countries with wealth over $274.9k per adult. The report appears causal up to these wealth scores.

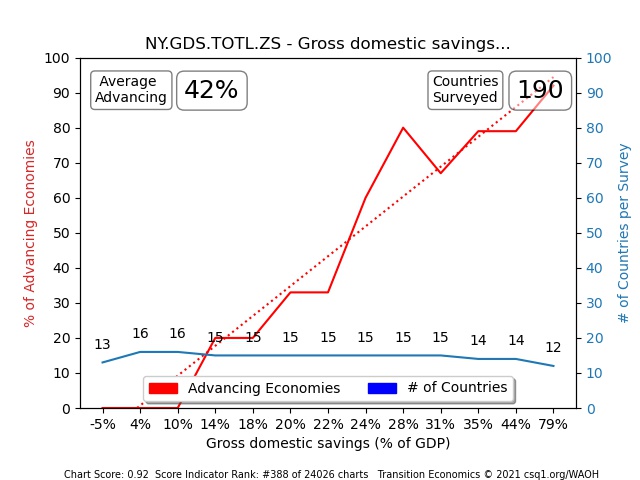

So, TE uses indicators that are known to be causal across almost 200 countries – like Trade Balance, Domestic Savings, and similar.

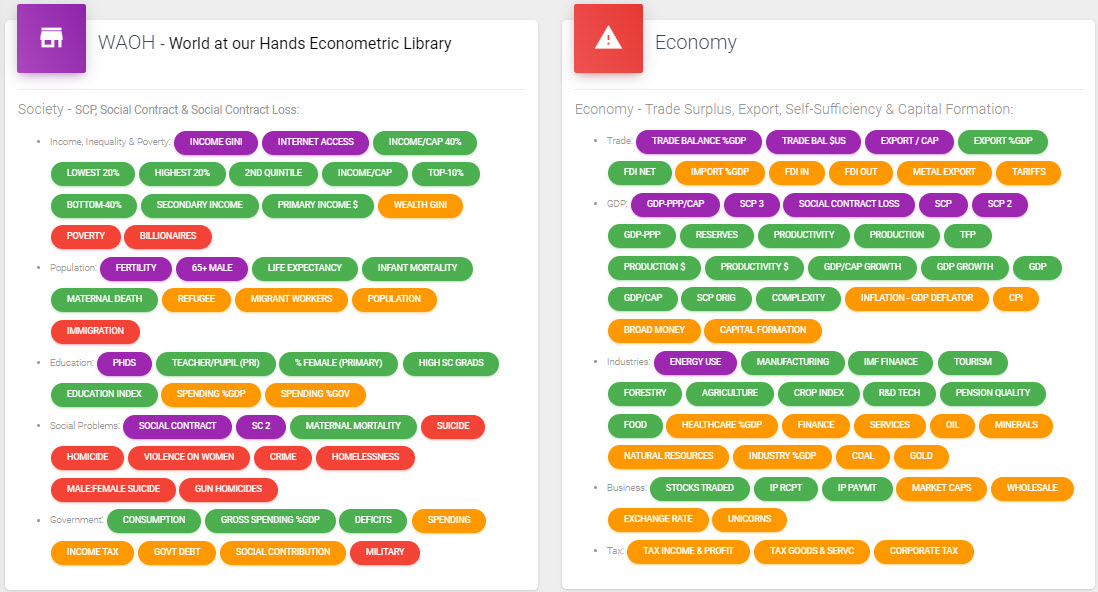

![]() Find hundreds of similar Causal, and not-so-causal, indicators and their TE proofs at the WAOH Civics Library. WAOH also curates a survey research “wishlist” for new indicators that evidence-based Civic Scientists might like to add to the existing measures that are already collected.

Find hundreds of similar Causal, and not-so-causal, indicators and their TE proofs at the WAOH Civics Library. WAOH also curates a survey research “wishlist” for new indicators that evidence-based Civic Scientists might like to add to the existing measures that are already collected.

Transition Economics Proof (TEP) Chart “scores” – are taken from frequency distribution (FD) charts created from indicator surveys from 28 to 220 nations – using a data science approach similar to Six Sigma and the Pareto Principle (the 80/20 Rule).

Why is “28 countries” the minimum permitted? Because, we want to see trendlines in the FD charts, which calls for a chart with no less than 4 data points; and, we also want each data point to compare no less than 7 countries so that we have as statistically significant a decision as can be offered by our often-small datasets. Surveys of more countries are better obviously, and data point comparisons of 10 countries or more offer more-truthful results.

TE isolates high-income countries in some reports, and mid and low-income countries in others; there are many ways to look at available data – but usually, TE surveys with more countries (120+) make better, more credible, reports.

Confirm any report here for yourself

TE is a science that makes “unsupported by data” opinions impossible. Anyone can confirm these survey results for themselves using public data and a spreadsheet.

We called our first scoring method – the Science of 70%; and the tutorial at this link explains how to create any TEP charts that you see here on the CSQ1.org website – for yourself – so that you don’t have to take our word for anything. You can also reach out to request any of our TEP chart source data at [email protected] (we take data from a hundred sources) and APIs are available to save your research teams from having to recalculate TEP chart data points and scores for yourself.

Data Science and Transition Economics

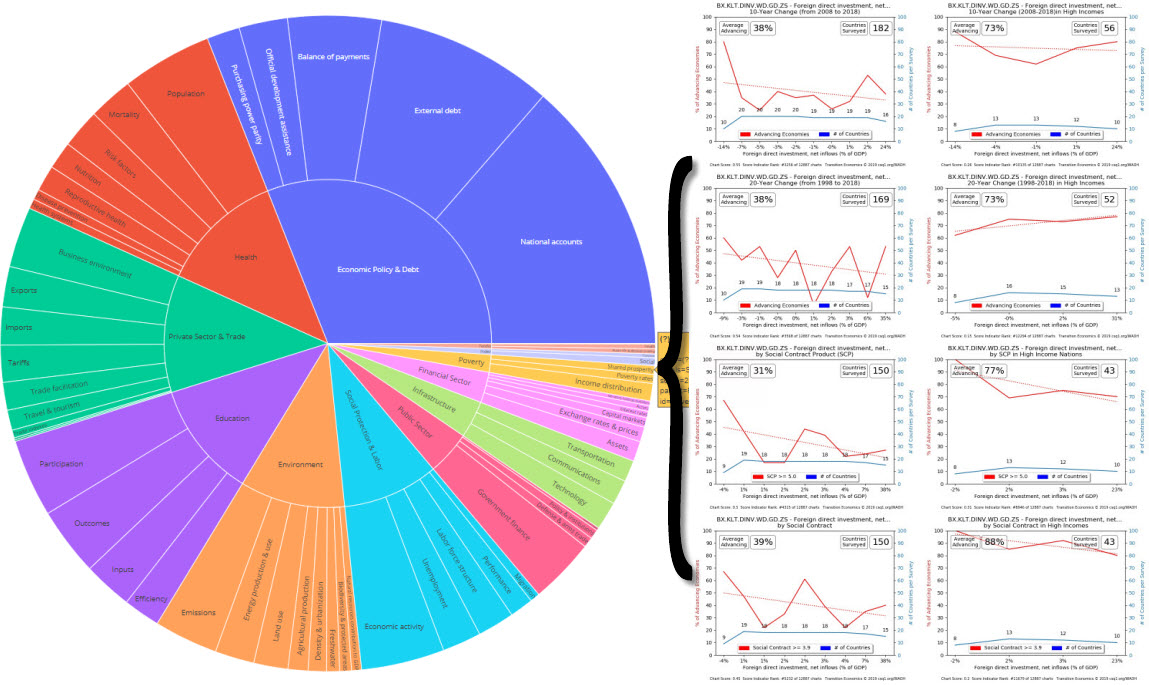

Data Science is an exciting new field in quantitative computing. Transition Economics develops leading-edge Jupyter Notebook, Python, MatPlotLib, and Javascript Charting & modeling tools like MEMS and WAOH (The World at Our Hands Report – TE’s Econometric Proofs Library). Tools and data visualizations provide new clarity and insight into the reliable management of successful economies and societies. See a sample of some of the highest-scoring of the 15,000 TEP reports that we curate in the tables and slideshow below

Data Science is an exciting new field in quantitative computing. Transition Economics develops leading-edge Jupyter Notebook, Python, MatPlotLib, and Javascript Charting & modeling tools like MEMS and WAOH (The World at Our Hands Report – TE’s Econometric Proofs Library). Tools and data visualizations provide new clarity and insight into the reliable management of successful economies and societies. See a sample of some of the highest-scoring of the 15,000 TEP reports that we curate in the tables and slideshow below

TEP Scores

TEP Scores

With new tools, come new capabilities. Each TEP chart is a consolidation of 15,000 records and 60 years of data too. Data science tools now permit us to process 10-TEP charts for 1,500 Indicators and Indexes in under an hour; easily scoring, sorting, and ranking Sustainable and Causal Indicators, separating them from the lion’s share of meaningless indicators like GDP, Disposable Income, Unemployment, Supply & Demand, Consumption economies, and so on.

High TEP-Score indicators and indexes have a high amplitude – a large difference between minimum low and maximum high values. Alternatively, statistics whose TEP surveys have small amplitudes, have little influence on economies. TE Scores average the individual TE amplitudes of all TEP surveys – see a sheet of TEP Charts in the image to the left here

Are you curious to know which reports are better than the United Nations HDI Report – for example? There are a dozen better indicators – and this technique can help improve future HDI Reports as well

Are you curious to know which reports are better than the United Nations HDI Report – for example? There are a dozen better indicators – and this technique can help improve future HDI Reports as well

Finding Data and Creating TE Causality Scores

An “indicator” is just a measure that has been collected similarly in many countries. Examples include Population, Longevity, Trade Balance, and 1500 other measures that are recorded and forwarded to data consolidators so that this data can be easily downloaded online by any of us who are reading this article.

Data Consolidators include the WHO, United Nations, the World Bank, OECD, Wiki lists, and hundreds of other providers and research bodies. Detail how-to questions are answered in our Science of 70% tutorial mentioned above.

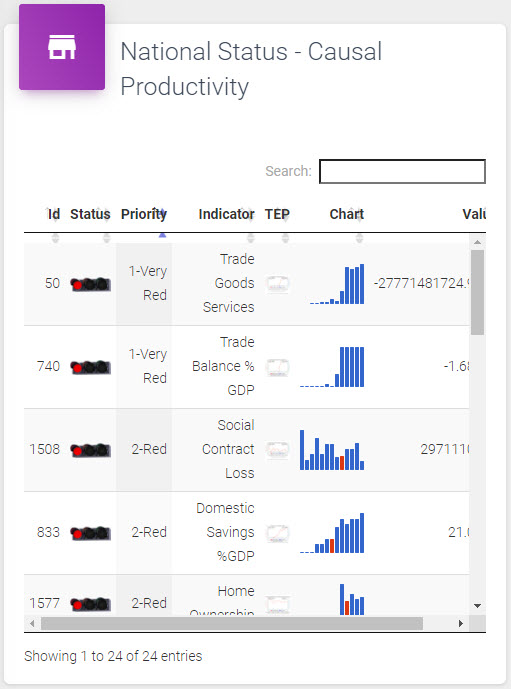

In addition to automating the creation of TEP Charts, the Science of 70%‘s “thresholds” permits us to understand whether a nation is collapsing or advancing too. See a Case Study example of this National Status approach here.

The WAOH Civics Library – is an evidence-based Public Civics Library (Library Symbol – OTWA), central Knowledgebase and Standard of Research, that curates and catalogs 60,000 TEP chart survey results along with metadata, APIs, MEMS A.I. and Machine Learning tools.

![]() Score – Each TEP Chart is scored by subtracting its maximum value from its minimum value (the chart’s “amplitude”). A TEP chart’s maximum possible score is 100% minus 0% – or 1.0, but indicator TEP surveys typically score between .6 and .7.

Score – Each TEP Chart is scored by subtracting its maximum value from its minimum value (the chart’s “amplitude”). A TEP chart’s maximum possible score is 100% minus 0% – or 1.0, but indicator TEP surveys typically score between .6 and .7.

Rank – is the importance of the report (by score) compared to all other TEP Reports

Click here to learn how to read TEP Charts

TEP “Sheets” – present many TEP Reports for a single indicator onto one sheet. Click on the image to the right here …

TEP “Sheets” – present many TEP Reports for a single indicator onto one sheet. Click on the image to the right here …

TEP Report Types – can include TEP (Trade Balance), Social Contract (SC), Social Contract Product (SCP), High-Income (HI) nations, Change over x years, Gini, Per Population, and so on.

TEP Sheet Scores – average all TEP scores on a TEP Sheet together, for one indicator.

Indexes – Indexes combine several indicators until an optimal causality is reached. The most causal reports are Indexes.

Data Quality, History, and Consistency

Consistency – Smaller countries can only afford to collect a smaller number of indicator measures, and not all measures are collected annually, some are collected intermittently (once every 3 to 5 years), and other measures are one-time collections without history.

History – Some data is recorded for a century in some cases – and even 200 years in the example of the USA’s GDP reports, while others started reporting in the 1960s, and more still began in the 1990s. PPP was used for the first time in 1990, so there won’t be PPP stats earlier than this.

Data Quality – Much time and effort is taken to gather and forward measures reliably. Embarrassing stats such as suicide, homelessness, wealth inequality, and infant mortality rates can be under-reported in many countries. The hiding of stats by embarrassed countries tends to be consistent and ubiquitous. If one nation is hiding or misreporting a statistic, there is a higher probability that all nations are hiding their true values for that indicator as well.

Curated Data and MEMS Dashboards

The number of TE Proof Reports and Report Types is always growing. Today, a typical “TEP Sheet” displays 20 TEP Report Types with TE XY Scatter Charts – and then MEMS AI (TE’s interactive AI Dashboard) also presents many additional interactive versions of each TEP Report – with an API service.

WAOH and MEMS are presently the only online source of Transition Economics data.

WAOH and MEMS are presently the only online source of Transition Economics data.

See Data Science at WAOH

By recording, sorting, and ranking the scores taken from tens of thousands of TEP Charts and TEP Sheets, we can confirm every indicator’s importance and probability of contributing to building a successful economy and society.

Indicators can also be aggregated so that multiple indicators can combine to create an index (see how indexes are built below). Index values can then be charted, scored, and ranked; and trending reports can explain changes in the index over time as far back as we have data.

The following table shows 1500+ indicators (and indexes) ranked by TEP Scores for Social Contract, 10-year Change, Trade Balance, Population, High-Income Nations, and combinations of these measures too, summarizing the scores collected from all frequency distribution reports.

These web-based tables permit us to resort them by column easily, and this analyzes important indicators and combinations straightforwardly for anyone.

| Indicator | TEP | TEP HIs | SCP | Soc Contract | GINI | Per Cap | SCP 2020 | SC 2020 | TEP-SCP | TEP-SCP HIs | TEP-SC | TEP-SC HIs | TEP-CAP | TEP-CAP HIs | TEP CAP SC | TEP CAP SC HIs | Mean All |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % Agro Land | 0.44 | 0.22 | 0.41 | 0.45 | 0.25 | 0.6 | 0.4 | 0.52 | 0.425 | 0.225 | 0.445 | 0.155 | 0.52 | 0.29 | 0.496666667 | 0.223333333 | 0.466 |

| % Arable Land | 0.43 | 0.51 | 0.57 | 0.47 | 0.37 | 0.42 | 0.46 | 0.51 | 0.5 | 0.395 | 0.45 | 0.29 | 0.425 | 0.425 | 0.44 | 0.306666667 | 0.496 |

| Abortion Rates | 0.39 | 0.44 | 0.45 | 0.42 | 0.52 | 0.19 | 0.42 | 0.59 | 0.42 | 0.28 | 0.405 | 0.23 | 0.29 | 0.28 | 0.333333333 | 0.193333333 | 0.42 |

| Access Electricity Rural | 0.4 | 0 | 0.52 | 0.64 | 0.31 | 0.47 | 0.5 | 0.48 | 0.46 | 0 | 0.52 | 0 | 0.435 | 0.21 | 0.503333333 | 0.14 | 0.576 |

| Access Electricity Urban | 0.46 | 0 | 0.51 | 0.65 | 0.32 | 0.49 | 0.51 | 0.42 | 0.485 | 0 | 0.555 | 0 | 0.475 | 0.21 | 0.533333333 | 0.14 | 0.606 |

| Account Balance % | 0.77 | 0.5 | 0.69 | 0.67 | 0.5 | 0.71 | 0.5 | 0.62 | 0.73 | 0.4 | 0.72 | 0.375 | 0.74 | 0.5 | 0.716666667 | 0.416666667 | 0.582 |

| Account Balance US$ | 0.94 | 0.62 | 0.85 | 0.85 | 0.34 | 0.84 | 0.92 | 0.69 | 0.895 | 0.48 | 0.895 | 0.435 | 0.89 | 0.62 | 0.876666667 | 0.496666667 | 0.876 |

| Adjusted Savings US$ | 0.67 | 0.29 | 0.75 | 0.87 | 0.34 | 0.94 | 0.83 | 0.67 | 0.71 | 0.335 | 0.77 | 0.27 | 0.805 | 0.37 | 0.826666667 | 0.33 | 0.726 |

| Adv Edu Labor % | 0.52 | 0.38 | 0.39 | 0.38 | 0.28 | 0.52 | 0.5 | 0.47 | 0.455 | 0.4 | 0.45 | 0.34 | 0.52 | 0.38 | 0.473333333 | 0.353333333 | 0.464 |

| Adv Edu. Labor Force | 0.41 | 0.33 | 0.36 | 0.48 | 0.21 | 0.49 | 0.5 | 0.53 | 0.385 | 0.29 | 0.445 | 0.365 | 0.45 | 0.355 | 0.46 | 0.37 | 0.432 |

| Ag Machinery | 0.79 | 0.26 | 0.92 | 0.92 | 0.44 | 0.61 | 0.92 | 0.75 | 0.855 | 0.3 | 0.855 | 0.255 | 0.7 | 0.34 | 0.773333333 | 0.31 | 0.716 |

| Age 65 + Male | 0.94 | 0.43 | 0.92 | 0.93 | 0.53 | 0.41 | 1 | 1 | 0.93 | 0.445 | 0.935 | 0.34 | 0.675 | 0.42 | 0.76 | 0.363333333 | 0.772 |

| Aged >80 Male as %Pop | 0.54 | 0.31 | 0.85 | 0.92 | 0.5 | 0.51 | 1 | 0.79 | 0.695 | 0.365 | 0.73 | 0.19 | 0.525 | 0.32 | 0.656666667 | 0.236666667 | 0.668 |

| Agri Forest Fish | 0.37 | 0.21 | 0.49 | 0.5 | 0.19 | 0.39 | 0.28 | 0.7 | 0.43 | 0.255 | 0.435 | 0.23 | 0.38 | 0.255 | 0.42 | 0.253333333 | 0.476 |

| Agri For-Fish Growth | 0.53 | 0.28 | 0.49 | 0.49 | 0.17 | 0.28 | 0.34 | 0.54 | 0.51 | 0.215 | 0.51 | 0.29 | 0.405 | 0.245 | 0.433333333 | 0.263333333 | 0.46 |

| Agri Irrigated | 0.5 | 0.13 | 0.71 | 0.64 | 0.4 | 0.44 | 0.62 | 0.42 | 0.605 | 0.125 | 0.57 | 0.19 | 0.47 | 0.17 | 0.526666667 | 0.196666667 | 0.505 |

| Agricultural Methane | 0.22 | 0.33 | 0.38 | 0.33 | 0.35 | 0.34 | 0.4 | 0.48 | 0.3 | 0.28 | 0.275 | 0.25 | 0.28 | 0.34 | 0.296666667 | 0.283333333 | 0.358 |

| Agricultural Methane | 0.49 | 0.11 | 0.47 | 0.57 | 0.28 | 0.45 | 0.51 | 0.73 | 0.48 | 0.125 | 0.53 | 0.17 | 0.47 | 0.235 | 0.503333333 | 0.233333333 | 0.526 |

| Agriculture % | 0.88 | 0.39 | 0.82 | 0.9 | 0.44 | 0.61 | 1 | 0.9 | 0.85 | 0.405 | 0.89 | 0.345 | 0.745 | 0.435 | 0.796666667 | 0.39 | 0.79 |

| Agro Land (km2) | 0.47 | 0.47 | 0.21 | 0.4 | 0.35 | 0.57 | 0.22 | 0.61 | 0.34 | 0.325 | 0.435 | 0.36 | 0.52 | 0.45 | 0.48 | 0.383333333 | 0.436 |

| Agro Machines | 0.69 | 0.3 | 0.8 | 0.83 | 0.67 | 0.62 | 0.83 | 0.57 | 0.745 | 0.225 | 0.76 | 0.235 | 0.655 | 0.46 | 0.713333333 | 0.363333333 | 0.598 |

| Aid DAC to Hungary | 0.29 | 0 | 0.31 | 0.52 | 0.3 | 0.26 | 0.33 | 0.09 | 0.3 | 0 | 0.405 | 0 | 0.275 | 0 | 0.356666667 | 0 | 0.37 |

| Aid Flows donors | 0.5 | 0.48 | 0.5 | 0.42 | 0.33 | 0.48 | 0.29 | 0.33 | 0.5 | 0.24 | 0.46 | 0.24 | 0.49 | 0.39 | 0.466666667 | 0.26 | 0.454 |

| Air Freight | 0.74 | 0.46 | 0.69 | 0.77 | 0.4 | 0.8 | 0.91 | 0.64 | 0.715 | 0.345 | 0.755 | 0.355 | 0.77 | 0.335 | 0.77 | 0.306666667 | 0.702 |

| Air Infrastructure | 0.59 | 0.4 | 0.67 | 0.74 | 0.44 | 0.88 | 0.77 | 0.6 | 0.63 | 0.305 | 0.665 | 0.325 | 0.735 | 0.325 | 0.736666667 | 0.3 | 0.644 |

| Air Pollution | 0.53 | 0.28 | 0.8 | 0.93 | 0.4 | 0.33 | 0.94 | 1 | 0.665 | 0.295 | 0.73 | 0.225 | 0.43 | 0.35 | 0.596666667 | 0.29 | 0.753333333 |

| Air Pollution %pop | 0.37 | 0.29 | 0.62 | 0.75 | 0.24 | 0.47 | 0.84 | 0.83 | 0.495 | 0.235 | 0.56 | 0.23 | 0.42 | 0.32 | 0.53 | 0.27 | 0.58 |

| Air Traffic | 0.58 | 0.13 | 0.67 | 0.67 | 0.44 | 0.62 | 0.71 | 0.54 | 0.625 | 0.155 | 0.625 | 0.19 | 0.6 | 0.17 | 0.623333333 | 0.196666667 | 0.618 |

| Alcohol (litres/yr) | 0.55 | 0.33 | 0.74 | 0.61 | 0.62 | 0.29 | 0.69 | 0.53 | 0.645 | 0.28 | 0.58 | 0.315 | 0.42 | 0.29 | 0.483333333 | 0.293333333 | 0.633333333 |

| Alcohol per Cap | 0.55 | 0.27 | 0.74 | 0.61 | 0.54 | 0.29 | 0.65 | 0.56 | 0.645 | 0.25 | 0.58 | 0.285 | 0.42 | 0.225 | 0.483333333 | 0.25 | 0.633333333 |

| Alt Convert Factor | 0.57 | 0.35 | 0.66 | 0.8 | 0.46 | 0.58 | 0.73 | 0.74 | 0.615 | 0.285 | 0.685 | 0.26 | 0.575 | 0.435 | 0.65 | 0.346666667 | 0.628 |

| Anemia <5 | 0.81 | 0.3 | 0.9 | 1 | 0.7 | 0.46 | 1 | 0.9 | 0.855 | 0.4 | 0.905 | 0.315 | 0.635 | 0.4 | 0.756666667 | 0.376666667 | 0.806 |

| Anemia in Pregancy | 0.47 | 0.45 | 0.78 | 0.78 | 0.55 | 0.39 | 0.66 | 0.7 | 0.625 | 0.41 | 0.625 | 0.36 | 0.43 | 0.435 | 0.546666667 | 0.38 | 0.71 |

| Anemia Non-preg | 0.66 | 0.42 | 0.76 | 0.74 | 0.53 | 0.39 | 0.75 | 0.82 | 0.71 | 0.4 | 0.7 | 0.39 | 0.525 | 0.42 | 0.596666667 | 0.4 | 0.726 |

| Anemia Women 15-49 | 0.61 | 0.42 | 0.76 | 0.74 | 0.53 | 0.39 | 0.73 | 0.78 | 0.685 | 0.4 | 0.675 | 0.39 | 0.5 | 0.42 | 0.58 | 0.4 | 0.73 |

| Annualized | 0.33 | 0.5 | 0.19 | 0.61 | 0.41 | 0.51 | 0.55 | 0.45 | 0.26 | 0.46 | 0.47 | 0.375 | 0.42 | 0.34 | 0.483333333 | 0.31 | 0.376666667 |

| Annualized | 0.37 | 0.39 | 0.39 | 0.65 | 0.34 | 0.62 | 0.46 | 0.38 | 0.38 | 0.3 | 0.51 | 0.28 | 0.495 | 0.39 | 0.546666667 | 0.316666667 | 0.47 |

| Aquaculture | 0.45 | 0.47 | 0.44 | 0.51 | 0.32 | 0.42 | 0.67 | 0.38 | 0.445 | 0.385 | 0.48 | 0.36 | 0.435 | 0.445 | 0.46 | 0.38 | 0.44 |

| Arab imports | 0.47 | 0.54 | 0.88 | 0.6 | 0.65 | 0.46 | 0.59 | 0.39 | 0.675 | 0.46 | 0.535 | 0.395 | 0.465 | 0.52 | 0.51 | 0.43 | 0.586 |

| Arable Land (hec) | 0.4 | 0.67 | 0.28 | 0.37 | 0.26 | 0.42 | 0.28 | 0.74 | 0.34 | 0.44 | 0.385 | 0.42 | 0.41 | 0.525 | 0.396666667 | 0.406666667 | 0.432 |

| Arable Land (hec/cap) | 0.42 | 0.38 | 0.38 | 0.61 | 0.28 | 0.43 | 0.26 | 0.74 | 0.4 | 0.35 | 0.515 | 0.34 | 0.425 | 0.35 | 0.486666667 | 0.333333333 | 0.494 |

| Arms Exports | 0.34 | 0.29 | 0.75 | 0.74 | 0.46 | 0.46 | 0.74 | 0.63 | 0.545 | 0.27 | 0.54 | 0.235 | 0.4 | 0.265 | 0.513333333 | 0.236666667 | 0.486 |

| Arms Import | 0.6 | 0.41 | 0.62 | 0.71 | 0.36 | 0.46 | 0.64 | 0.45 | 0.61 | 0.3 | 0.655 | 0.24 | 0.53 | 0.325 | 0.59 | 0.24 | 0.632 |

| ATMs | 0.69 | 0.13 | 0.77 | 0.77 | 0.35 | 0.59 | 0.85 | 0.62 | 0.73 | 0.255 | 0.73 | 0.165 | 0.64 | 0.215 | 0.683333333 | 0.21 | 0.71 |

| Bachelors Female | 0.86 | 0.1 | 0.75 | 0.82 | 0.5 | 0.48 | 0.78 | 0.69 | 0.805 | 0.255 | 0.84 | 0.13 | 0.67 | 0.26 | 0.72 | 0.226666667 | 0.81 |

| Bad Loans | 0.64 | 0.21 | 0.76 | 0.83 | 0.36 | 0.56 | 0.94 | 0.82 | 0.7 | 0.265 | 0.735 | 0.215 | 0.6 | 0.32 | 0.676666667 | 0.286666667 | 0.6825 |

| Bal Budgets %GDP | 0.6 | 0.42 | 0.47 | 0.68 | 0.29 | 0.42 | 0.49 | 0.52 | 0.535 | 0.305 | 0.64 | 0.31 | 0.51 | 0.4 | 0.566666667 | 0.333333333 | 0.583333333 |

| Bank Branches | 0.55 | 0.3 | 0.5 | 0.67 | 0.26 | 0.61 | 0.54 | 0.54 | 0.525 | 0.3 | 0.61 | 0.265 | 0.58 | 0.4 | 0.61 | 0.343333333 | 0.62 |

| Bank Capital:Asset Ratio | 0.5 | 0.23 | 0.3 | 0.42 | 0.38 | 0.51 | 0.55 | 0.55 | 0.4 | 0.205 | 0.46 | 0.215 | 0.505 | 0.385 | 0.476666667 | 0.323333333 | 0.3925 |

| Bank Reserves | 0.5 | 0.07 | 0.6 | 0.71 | 0.21 | 0.22 | 0.58 | 0.72 | 0.55 | 0.035 | 0.605 | 0.035 | 0.36 | 0.07 | 0.476666667 | 0.046666667 | 0.5625 |

| Barter Index | 0.73 | 0.33 | 0.55 | 0.43 | 0.5 | 0.31 | 0.59 | 0.35 | 0.64 | 0.325 | 0.58 | 0.21 | 0.52 | 0.415 | 0.49 | 0.306666667 | 0.508 |

| Battered Women | 0.45 | 0 | 0.33 | 0.33 | 0.19 | 0.17 | 0.15 | 0.09 | 0.39 | 0 | 0.39 | 0 | 0.31 | 0 | 0.316666667 | 0 | 0.37 |

| Beatings | 0.33 | 0 | 0.38 | 0.25 | 0.17 | 0.3 | 0.14 | 0.08 | 0.355 | 0 | 0.29 | 0 | 0.315 | 0 | 0.293333333 | 0 | 0.32 |

| Big Mac Index | 0.5 | 0 | 0.29 | 0.64 | 0.35 | 0.42 | 0.63 | 0.8 | 0.395 | 0 | 0.57 | 0 | 0.46 | 0 | 0.52 | 0 | 0.3875 |

| Billionaires Per Nation | 0.28 | 0.5 | 0.53 | 0.39 | 0.69 | 0.57 | 0.62 | 0.44 | 0.405 | 0.31 | 0.335 | 0.305 | 0.425 | 0.325 | 0.413333333 | 0.253333333 | 0.394 |

| Birth rate, crude | 0.69 | 0.38 | 0.81 | 0.94 | 0.47 | 0.5 | 0.76 | 0.6 | 0.75 | 0.31 | 0.815 | 0.315 | 0.595 | 0.4 | 0.71 | 0.35 | 0.71 |

| Births Lost | 0.52 | 0.59 | 0.34 | 0.42 | 0.38 | 0.56 | 0.5 | 0.16 | 0.43 | 0.46 | 0.47 | 0.405 | 0.54 | 0.595 | 0.5 | 0.47 | 0.398 |

| Borrowers | 0.47 | 0 | 0.5 | 0.7 | 0.23 | 0.47 | 0.7 | 0.36 | 0.485 | 0 | 0.585 | 0 | 0.47 | 0 | 0.546666667 | 0 | 0.5225 |

| Bribery | 0.36 | 0 | 0.26 | 0.56 | 0.33 | 0.37 | 0.54 | 0.4 | 0.31 | 0 | 0.46 | 0 | 0.365 | 0 | 0.43 | 0 | 0.37 |

| Broad Money | 0.57 | 0.4 | 0.69 | 0.77 | 0.4 | 0.57 | 0.69 | 0.53 | 0.63 | 0.2 | 0.67 | 0.2 | 0.57 | 0.45 | 0.636666667 | 0.3 | 0.618 |

| Broad Money Growth | 0.62 | 0.62 | 0.5 | 0.41 | 0.33 | 0.58 | 0.44 | 0.5 | 0.56 | 0.31 | 0.515 | 0.31 | 0.6 | 0.38 | 0.536666667 | 0.253333333 | 0.42 |

| Broad Money LCU | 0.53 | 0.13 | 0.38 | 0.38 | 0.3 | 0.43 | 0.5 | 0.32 | 0.455 | 0.065 | 0.455 | 0.065 | 0.48 | 0.21 | 0.446666667 | 0.14 | 0.396 |

| Broad Money Ratio | 0.36 | 0.5 | 0.33 | 0.45 | 0.27 | 0.24 | 0.47 | 0.36 | 0.345 | 0.25 | 0.405 | 0.25 | 0.3 | 0.34 | 0.35 | 0.226666667 | 0.408 |

| Budget Deficits | 0.85 | 0.45 | 0.67 | 0.53 | 0.61 | 0.77 | 0.5 | 0.5 | 0.76 | 0.475 | 0.69 | 0.35 | 0.81 | 0.425 | 0.716666667 | 0.366666667 | 0.683333333 |

| Bus Start days | 0.37 | 0.46 | 0.58 | 0.6 | 0.32 | 0.41 | 0.53 | 0.51 | 0.475 | 0.515 | 0.485 | 0.375 | 0.39 | 0.44 | 0.46 | 0.39 | 0.455 |

| Bus Start Male Days | 0.46 | 0.57 | 0.54 | 0.61 | 0.33 | 0.41 | 0.57 | 0.55 | 0.5 | 0.57 | 0.535 | 0.43 | 0.435 | 0.495 | 0.493333333 | 0.426666667 | 0.47 |

| Bus. Start Fem. Days | 0.47 | 0.53 | 0.58 | 0.6 | 0.33 | 0.41 | 0.52 | 0.51 | 0.525 | 0.555 | 0.535 | 0.43 | 0.44 | 0.475 | 0.493333333 | 0.426666667 | 0.48 |

| Business Disclosure Index | 0.41 | 0.27 | 0.36 | 0.36 | 0.31 | 0.39 | 0.55 | 0.3 | 0.385 | 0.235 | 0.385 | 0.225 | 0.4 | 0.285 | 0.386666667 | 0.25 | 0.3575 |

| Cap Formation | 0.36 | 0.13 | 0.55 | 0.42 | 0.34 | 0.32 | 0.56 | 0.46 | 0.455 | 0.145 | 0.39 | 0.19 | 0.34 | 0.165 | 0.366666667 | 0.193333333 | 0.476 |

| Cap Formation | 0.36 | 0.3 | 0.6 | 0.59 | 0.28 | 0.37 | 0.57 | 0.53 | 0.48 | 0.3 | 0.475 | 0.275 | 0.365 | 0.29 | 0.44 | 0.276666667 | 0.504 |

| Cap Formation | 0.41 | 0.14 | 0.49 | 0.49 | 0.34 | 0.36 | 0.5 | 0.46 | 0.45 | 0.14 | 0.45 | 0.195 | 0.385 | 0.175 | 0.42 | 0.2 | 0.422 |

| Cap Formation | 0.49 | 0.37 | 0.53 | 0.52 | 0.47 | 0.41 | 0.54 | 0.65 | 0.51 | 0.29 | 0.505 | 0.245 | 0.45 | 0.26 | 0.473333333 | 0.213333333 | 0.554 |

| Cap Formation | 0.49 | 0.08 | 0.4 | 0.49 | 0.38 | 0.41 | 0.46 | 0.36 | 0.445 | 0.24 | 0.49 | 0.23 | 0.45 | 0.215 | 0.463333333 | 0.27 | 0.466 |

| Cap Formation | 0.58 | 0.46 | 0.45 | 0.59 | 0.23 | 0.31 | 0.56 | 0.53 | 0.515 | 0.295 | 0.585 | 0.355 | 0.445 | 0.38 | 0.493333333 | 0.336666667 | 0.512 |

| Cap Formation | 0.76 | 0.62 | 0.8 | 0.87 | 0.3 | 0.86 | 0.85 | 0.62 | 0.78 | 0.48 | 0.815 | 0.5 | 0.81 | 0.425 | 0.83 | 0.41 | 0.754 |

| Cap Formation | 0.76 | 0.5 | 0.73 | 0.87 | 0.3 | 0.88 | 0.85 | 0.62 | 0.745 | 0.39 | 0.815 | 0.44 | 0.82 | 0.4 | 0.836666667 | 0.393333333 | 0.756 |

| Cap Formation | 0.87 | 0.4 | 0.86 | 0.83 | 0.34 | 0.92 | 0.83 | 0.57 | 0.865 | 0.34 | 0.85 | 0.39 | 0.895 | 0.41 | 0.873333333 | 0.4 | 0.75 |

| Cap Formation | 0.88 | 0.38 | 0.86 | 0.83 | 0.34 | 0.83 | 0.87 | 0.67 | 0.87 | 0.33 | 0.855 | 0.38 | 0.855 | 0.34 | 0.846666667 | 0.353333333 | 0.736 |

| Capital | 0.59 | 0.29 | 0.67 | 0.48 | 0.44 | 0.4 | 0.63 | 0.63 | 0.63 | 0.355 | 0.535 | 0.23 | 0.495 | 0.26 | 0.49 | 0.23 | 0.482 |

| Capital Formation $ | 0.55 | 0.42 | 0.55 | 0.53 | 0.32 | 0.35 | 0.56 | 0.47 | 0.55 | 0.36 | 0.54 | 0.335 | 0.45 | 0.35 | 0.476666667 | 0.316666667 | 0.484 |

| Capital Formation % | 0.38 | 0.22 | 0.56 | 0.49 | 0.21 | 0.41 | 0.37 | 0.5 | 0.47 | 0.31 | 0.435 | 0.235 | 0.395 | 0.335 | 0.426666667 | 0.306666667 | 0.482 |

| Capture Fisheries | 0.33 | 0.24 | 0.47 | 0.41 | 0.44 | 0.37 | 0.5 | 0.41 | 0.4 | 0.25 | 0.37 | 0.235 | 0.35 | 0.39 | 0.37 | 0.336666667 | 0.482 |

| Cause Death non-comncble | 0.57 | 0.36 | 0.8 | 0.85 | 0.6 | 0.55 | 0.88 | 0.75 | 0.685 | 0.39 | 0.71 | 0.215 | 0.56 | 0.37 | 0.656666667 | 0.27 | 0.74 |

| Cause of Death disease | 0.6 | 0.24 | 0.81 | 0.9 | 0.6 | 0.36 | 0.76 | 0.65 | 0.705 | 0.28 | 0.75 | 0.245 | 0.48 | 0.33 | 0.62 | 0.303333333 | 0.77 |

| Cause of Death Registry | 0.4 | 0.12 | 0.49 | 0.46 | 0.36 | 0.37 | 0.56 | 0.41 | 0.445 | 0.3 | 0.43 | 0.14 | 0.385 | 0.25 | 0.41 | 0.22 | 0.462 |

| Cell subscriptions | 0.8 | 0.54 | 0.62 | 0.59 | 0.41 | 0.47 | 0.69 | 0.5 | 0.71 | 0.41 | 0.695 | 0.42 | 0.635 | 0.445 | 0.62 | 0.396666667 | 0.652 |

| Cell Subsribers | 0.37 | 0.62 | 0.35 | 0.38 | 0.34 | 0.69 | 0.43 | 0.25 | 0.36 | 0.425 | 0.375 | 0.425 | 0.53 | 0.6 | 0.48 | 0.476666667 | 0.334 |

| Cereal Land | 0.41 | 0.35 | 0.21 | 0.25 | 0.31 | 0.41 | 0.27 | 0.64 | 0.31 | 0.29 | 0.33 | 0.265 | 0.41 | 0.295 | 0.356666667 | 0.256666667 | 0.384 |

| Cereal tons | 0.35 | 0.35 | 0.35 | 0.29 | 0.38 | 0.52 | 0.31 | 0.38 | 0.35 | 0.25 | 0.32 | 0.3 | 0.435 | 0.35 | 0.386666667 | 0.316666667 | 0.37 |

| Cereal Yield | 0.81 | 0.29 | 0.73 | 0.92 | 0.41 | 0.51 | 0.92 | 0.85 | 0.77 | 0.265 | 0.865 | 0.31 | 0.66 | 0.29 | 0.746666667 | 0.303333333 | 0.648 |

| Changes | 0.46 | 0 | 0.26 | 0.4 | 0.33 | 0.31 | 0.26 | 0.24 | 0.36 | 0 | 0.43 | 0 | 0.385 | 0 | 0.39 | 0 | 0.378 |

| Changes | 0.58 | 0.24 | 0.61 | 0.61 | 0.44 | 0.73 | 0.63 | 0.6 | 0.595 | 0.225 | 0.595 | 0.31 | 0.655 | 0.265 | 0.64 | 0.303333333 | 0.614 |

| Child | 0.27 | 0 | 0.18 | 0.16 | 0.38 | 0.5 | 0.25 | 0.09 | 0.225 | 0 | 0.215 | 0 | 0.385 | 0 | 0.31 | 0 | 0.203333333 |

| Child Empl Manuf | 0.36 | 0 | 0.14 | 0.14 | 0.38 | 0.33 | 0.18 | 0.08 | 0.25 | 0 | 0.25 | 0 | 0.345 | 0 | 0.276666667 | 0 | 0.213333333 |

| Child w. 1 Parent | 0.41 | 0.4 | 0.41 | 0.16 | 0.53 | 0.36 | 0.15 | 0.41 | 0.41 | 0.33 | 0.285 | 0.285 | 0.385 | 0.335 | 0.31 | 0.28 | 0.355 |

| Child w. 2 Parents | 0.44 | 0.52 | 0.5 | 0.27 | 0.5 | 0.41 | 0.25 | 0.32 | 0.47 | 0.475 | 0.355 | 0.385 | 0.425 | 0.455 | 0.373333333 | 0.386666667 | 0.4275 |

| Children | 0.46 | 0 | 0.36 | 0.56 | 0.3 | 0.36 | 0.42 | 0.08 | 0.41 | 0 | 0.51 | 0 | 0.41 | 0 | 0.46 | 0 | 0.42 |

| Christianity | 0.41 | 0.36 | 0.4 | 0.36 | 0.34 | 0.37 | 0.43 | 0.44 | 0.405 | 0.305 | 0.385 | 0.33 | 0.39 | 0.295 | 0.38 | 0.296666667 | 0.39 |

| Claims Govt | 0.52 | 0.21 | 0.5 | 0.61 | 0.5 | 0.37 | 0.62 | 0.33 | 0.51 | 0.105 | 0.565 | 0.105 | 0.445 | 0.25 | 0.5 | 0.166666667 | 0.474 |

| Claims Other | 0.25 | 0.21 | 0.26 | 0.46 | 0.15 | 0.3 | 0.38 | 0.25 | 0.255 | 0.105 | 0.355 | 0.105 | 0.275 | 0.235 | 0.336666667 | 0.156666667 | 0.34 |

| Claims Priv. Sector | 0.28 | 0.19 | 0.3 | 0.45 | 0.36 | 0.36 | 0.26 | 0.24 | 0.29 | 0.095 | 0.365 | 0.095 | 0.32 | 0.295 | 0.363333333 | 0.196666667 | 0.346 |

| Clean Fuel Tech | 0.83 | 0.62 | 0.7 | 0.79 | 0.41 | 0.49 | 0.93 | 0.77 | 0.765 | 0.475 | 0.81 | 0.315 | 0.66 | 0.5 | 0.703333333 | 0.336666667 | 0.77 |

| Clothing Manuftg | 0.56 | 0.33 | 0.62 | 0.64 | 0.32 | 0.5 | 0.56 | 0.6 | 0.59 | 0.425 | 0.6 | 0.365 | 0.53 | 0.415 | 0.566666667 | 0.41 | 0.618 |

| CO2 Emissions | 0.36 | 0.19 | 0.61 | 0.63 | 0.36 | 0.57 | 0.4 | 0.53 | 0.485 | 0.2 | 0.495 | 0.22 | 0.465 | 0.21 | 0.52 | 0.223333333 | 0.536 |

| CO2 emissions | 0.48 | 0.3 | 0.54 | 0.48 | 0.34 | 0.47 | 0.64 | 0.7 | 0.51 | 0.3 | 0.48 | 0.235 | 0.475 | 0.265 | 0.476666667 | 0.233333333 | 0.502 |

| CO2 emissions | 0.49 | 0.4 | 0.65 | 0.69 | 0.47 | 0.33 | 0.52 | 0.44 | 0.57 | 0.305 | 0.59 | 0.3 | 0.41 | 0.435 | 0.503333333 | 0.356666667 | 0.504 |

| CO2 emissions | 0.5 | 0.56 | 0.53 | 0.47 | 0.47 | 0.45 | 0.64 | 0.36 | 0.515 | 0.445 | 0.485 | 0.405 | 0.475 | 0.445 | 0.473333333 | 0.38 | 0.562 |

| CO2 emissions | 0.58 | 0.33 | 0.74 | 0.53 | 0.59 | 0.8 | 0.65 | 0.42 | 0.66 | 0.27 | 0.555 | 0.29 | 0.69 | 0.285 | 0.636666667 | 0.273333333 | 0.634 |

| CO2 emissions | 0.64 | 0.43 | 0.69 | 0.78 | 0.37 | 0.84 | 0.88 | 0.67 | 0.665 | 0.365 | 0.71 | 0.33 | 0.74 | 0.43 | 0.753333333 | 0.363333333 | 0.682 |

| CO2 emissions | 0.64 | 0.43 | 0.58 | 0.72 | 0.24 | 0.67 | 0.84 | 0.67 | 0.61 | 0.24 | 0.68 | 0.26 | 0.655 | 0.48 | 0.676666667 | 0.35 | 0.664 |

| CO2 emissions | 0.8 | 0.62 | 0.67 | 0.73 | 0.47 | 0.79 | 0.69 | 0.62 | 0.735 | 0.425 | 0.765 | 0.435 | 0.795 | 0.535 | 0.773333333 | 0.44 | 0.68 |

| CO2 emissions | 0.93 | 0.53 | 0.67 | 0.69 | 0.47 | 0.93 | 0.73 | 0.5 | 0.8 | 0.405 | 0.81 | 0.39 | 0.93 | 0.41 | 0.85 | 0.356666667 | 0.7 |

| CO2 emissions % | 0.25 | 0.26 | 0.54 | 0.63 | 0.41 | 0.46 | 0.52 | 0.41 | 0.395 | 0.27 | 0.44 | 0.255 | 0.355 | 0.245 | 0.446666667 | 0.246666667 | 0.5 |

| CO2 emissions/cap | 0.87 | 0.41 | 0.85 | 0.87 | 0.5 | 0.73 | 0.92 | 0.92 | 0.86 | 0.455 | 0.87 | 0.395 | 0.8 | 0.495 | 0.823333333 | 0.456666667 | 0.776 |

| CO2 Intensity | 0.36 | 0.25 | 0.51 | 0.54 | 0.4 | 0.65 | 0.45 | 0.4 | 0.435 | 0.215 | 0.45 | 0.25 | 0.505 | 0.285 | 0.516666667 | 0.273333333 | 0.514 |

| Coal | 0.5 | 0.16 | 0.37 | 0.58 | 0.32 | 0.4 | 0.37 | 0.42 | 0.435 | 0.16 | 0.54 | 0.175 | 0.45 | 0.12 | 0.493333333 | 0.143333333 | 0.44 |

| Coal Electricity | 0.31 | 0.33 | 0.47 | 0.5 | 0.14 | 0.78 | 0.61 | 0.5 | 0.39 | 0.26 | 0.405 | 0.3 | 0.545 | 0.33 | 0.53 | 0.31 | 0.5 |

| Comm. Imports $US | 0.82 | 0.42 | 0.93 | 0.93 | 0.32 | 0.9 | 0.92 | 0.73 | 0.875 | 0.4 | 0.875 | 0.335 | 0.86 | 0.46 | 0.883333333 | 0.39 | 0.846 |

| Communications | 0.49 | 0.55 | 0.6 | 0.48 | 0.32 | 0.43 | 0.47 | 0.56 | 0.545 | 0.545 | 0.485 | 0.465 | 0.46 | 0.465 | 0.466666667 | 0.436666667 | 0.522 |

| Compound Inflation | 0.33 | 0.42 | 0.6 | 0.73 | 0.28 | 0.27 | 0.52 | 0.53 | 0.465 | 0.42 | 0.53 | 0.41 | 0.3 | 0.42 | 0.443333333 | 0.413333333 | 0.498 |

| Compulsory | 0.6 | 0.22 | 0.53 | 0.48 | 0.32 | 0.62 | 0.5 | 0.45 | 0.565 | 0.295 | 0.54 | 0.175 | 0.61 | 0.36 | 0.566666667 | 0.283333333 | 0.516 |

| Computer Service | 0.57 | 0.24 | 0.67 | 0.59 | 0.44 | 0.48 | 0.33 | 0.35 | 0.62 | 0.33 | 0.58 | 0.245 | 0.525 | 0.275 | 0.546666667 | 0.266666667 | 0.518 |

| Computer Services | 0.4 | 0.29 | 0.73 | 0.54 | 0.34 | 0.45 | 0.61 | 0.35 | 0.565 | 0.31 | 0.47 | 0.27 | 0.425 | 0.335 | 0.463333333 | 0.306666667 | 0.478 |

| Computer Services | 0.68 | 0.35 | 0.87 | 0.81 | 0.44 | 0.5 | 0.62 | 0.54 | 0.775 | 0.385 | 0.745 | 0.3 | 0.59 | 0.4 | 0.663333333 | 0.35 | 0.616 |

| Condom Use Female | 0.3 | 0 | 0.27 | 0.25 | 0.38 | 0.25 | 0.38 | 0.12 | 0.285 | 0 | 0.275 | 0 | 0.275 | 0 | 0.266666667 | 0 | 0.273333333 |

| Condom Use Male | 0.23 | 0 | 0.17 | 0.17 | 0.16 | 0.23 | 0.1 | 0 | 0.2 | 0 | 0.2 | 0 | 0.23 | 0 | 0.21 | 0 | 0.19 |

| Consumption LCU | 0.4 | 0.29 | 0.56 | 0.49 | 0.32 | 0.39 | 0.4 | 0.59 | 0.48 | 0.25 | 0.445 | 0.27 | 0.395 | 0.17 | 0.426666667 | 0.196666667 | 0.468 |

| Consumption per GDP | 1 | 0.78 | 0.69 | 0.67 | 0.41 | 0.42 | 0.7 | 0.7 | 0.845 | 0.58 | 0.835 | 0.49 | 0.71 | 0.57 | 0.696666667 | 0.446666667 | 0.654 |

| Consumption Private | 0.56 | 0.15 | 0.71 | 0.75 | 0.34 | 0.56 | 0.59 | 0.71 | 0.635 | 0.385 | 0.655 | 0.265 | 0.56 | 0.37 | 0.623333333 | 0.373333333 | 0.59 |

| Consumption US$ | 0.72 | 0.5 | 0.69 | 0.85 | 0.44 | 0.87 | 0.77 | 0.62 | 0.705 | 0.39 | 0.785 | 0.375 | 0.795 | 0.415 | 0.813333333 | 0.36 | 0.686 |

| Consumption US$ | 0.81 | 0.3 | 0.67 | 0.83 | 0.5 | 0.84 | 0.75 | 0.67 | 0.74 | 0.29 | 0.82 | 0.305 | 0.825 | 0.265 | 0.826666667 | 0.28 | 0.676 |

| Consumption/Cap | 0.36 | 0.3 | 0.62 | 0.54 | 0.37 | 0.33 | 0.6 | 0.41 | 0.49 | 0.225 | 0.45 | 0.25 | 0.345 | 0.36 | 0.41 | 0.306666667 | 0.45 |

| Container Traffic | 0.56 | 0.55 | 0.46 | 0.58 | 0.4 | 0.59 | 0.71 | 0.6 | 0.51 | 0.395 | 0.57 | 0.32 | 0.575 | 0.425 | 0.576666667 | 0.313333333 | 0.4725 |

| Contraceptive % Fem | 0.6 | 0.37 | 0.6 | 0.8 | 0.38 | 0.53 | 0.67 | 0.54 | 0.6 | 0.32 | 0.7 | 0.23 | 0.565 | 0.365 | 0.643333333 | 0.273333333 | 0.678 |

| Contract Enforcmt | 0.32 | 0.6 | 0.5 | 0.51 | 0.35 | 0.34 | 0.47 | 0.24 | 0.41 | 0.46 | 0.415 | 0.425 | 0.33 | 0.49 | 0.39 | 0.41 | 0.48 |

| Contributing | 0.66 | 0.21 | 0.9 | 0.84 | 0.47 | 0.78 | 0.92 | 0.9 | 0.78 | 0.255 | 0.75 | 0.27 | 0.72 | 0.315 | 0.76 | 0.32 | 0.788 |

| Corp. Depreciation US$ | 0.79 | 0.5 | 0.77 | 0.85 | 0.41 | 0.86 | 0.87 | 0.69 | 0.78 | 0.46 | 0.82 | 0.44 | 0.825 | 0.42 | 0.833333333 | 0.406666667 | 0.77 |

| Corruption Perception | 0.81 | 0.38 | 0.86 | 0.92 | 0.44 | 0.42 | 0.9 | 0.9 | 0.835 | 0.33 | 0.865 | 0.225 | 0.615 | 0.335 | 0.716666667 | 0.246666667 | 0.863333333 |

| Cost of Living Ratio | 0.67 | 0.21 | 0.88 | 0.77 | 0.53 | 0.5 | 1 | 1 | 0.775 | 0.305 | 0.72 | 0.205 | 0.585 | 0.255 | 0.646666667 | 0.236666667 | 0.773333333 |

| Cost to Export | 0.6 | 0.39 | 0.94 | 0.82 | 0.59 | 0.7 | 0.88 | 0.65 | 0.77 | 0.385 | 0.71 | 0.265 | 0.65 | 0.345 | 0.706666667 | 0.276666667 | 0.786666667 |

| Country Complexity | 0.6 | 0.46 | 0.85 | 0.81 | 0.71 | 0.61 | 0.93 | 0.85 | 0.725 | 0.495 | 0.705 | 0.355 | 0.605 | 0.3 | 0.673333333 | 0.283333333 | 0.622 |

| Coverage | 0.38 | 0 | 0.33 | 0.38 | 0.24 | 0.5 | 0.33 | 0.09 | 0.355 | 0 | 0.38 | 0 | 0.44 | 0 | 0.42 | 0 | 0.363333333 |

| CPI | 0.59 | 0.38 | 0.62 | 0.73 | 0.32 | 0.41 | 0.55 | 0.7 | 0.605 | 0.28 | 0.66 | 0.275 | 0.5 | 0.34 | 0.576666667 | 0.283333333 | 0.584 |

| CPIA | 0.2 | 0 | 0.12 | 0.19 | 0.25 | 0.31 | 0.29 | 0.06 | 0.16 | 0 | 0.195 | 0 | 0.255 | 0 | 0.233333333 | 0 | 0.17 |

| CPIA | 0.23 | 0 | 0.2 | 0.35 | 0.12 | 0.31 | 0.12 | 0.06 | 0.215 | 0 | 0.29 | 0 | 0.27 | 0 | 0.296666667 | 0 | 0.195 |

| CPIA | 0.25 | 0 | 0 | 0 | 0 | 0.23 | 0 | 0 | 0.125 | 0 | 0.125 | 0 | 0.24 | 0 | 0.16 | 0 | 0.07 |

| CPIA | 0.25 | 0 | 0.15 | 0.2 | 0.1 | 0.31 | 0.17 | 0.07 | 0.2 | 0 | 0.225 | 0 | 0.28 | 0 | 0.253333333 | 0 | 0.2 |

| CPIA Trade Rating | 0.24 | 0 | 0.5 | 1 | 0.44 | 0.23 | 0 | 0.03 | 0.37 | 0 | 0.62 | 0 | 0.235 | 0 | 0.49 | 0 | 0.435 |

| Credit %GDP | 0.76 | 0.1 | 0.85 | 0.92 | 0.32 | 0.39 | 0.92 | 0.69 | 0.805 | 0.19 | 0.84 | 0.24 | 0.575 | 0.24 | 0.69 | 0.286666667 | 0.712 |

| Credit Private % GDP | 0.76 | 0.1 | 0.85 | 0.92 | 0.38 | 0.33 | 0.92 | 0.77 | 0.805 | 0.19 | 0.84 | 0.24 | 0.545 | 0.205 | 0.67 | 0.263333333 | 0.682 |

| Credit Registry | 0.68 | 0 | 0.52 | 0.65 | 0.5 | 0.47 | 0.52 | 0.27 | 0.6 | 0.105 | 0.665 | 0.17 | 0.575 | 0 | 0.6 | 0.113333333 | 0.6075 |

| Crime & Theft | 0.6 | 0.52 | 0.67 | 0.68 | 0.44 | 0.38 | 0.64 | 0.67 | 0.635 | 0.445 | 0.64 | 0.32 | 0.49 | 0.57 | 0.553333333 | 0.42 | 0.65 |

| Crop Index | 0.4 | 0.21 | 0.64 | 0.73 | 0.53 | 0.25 | 0.82 | 0.65 | 0.52 | 0.315 | 0.565 | 0.305 | 0.325 | 0.255 | 0.46 | 0.303333333 | 0.546 |

| Cropland | 0.45 | 0.54 | 0.41 | 0.46 | 0.6 | 0.61 | 0.47 | 0.38 | 0.43 | 0.52 | 0.455 | 0.435 | 0.53 | 0.55 | 0.506666667 | 0.476666667 | 0.452 |

| Custom Process Burden | 0.94 | 0.41 | 0.79 | 0.85 | 0.38 | 0.55 | 1 | 0.92 | 0.865 | 0.415 | 0.895 | 0.295 | 0.745 | 0.35 | 0.78 | 0.293333333 | 0.775 |

| Customs Export | 0.34 | 0 | 0.67 | 0.75 | 0.47 | 0.29 | 0.47 | 0.29 | 0.505 | 0 | 0.545 | 0 | 0.315 | 0 | 0.46 | 0 | 0.4525 |

| Customs/Import Duties | 0.67 | 0.26 | 0.71 | 0.75 | 0.49 | 0.67 | 0.82 | 0.67 | 0.69 | 0.355 | 0.71 | 0.265 | 0.67 | 0.28 | 0.696666667 | 0.276666667 | 0.516 |

| Customs/Import Duties | 0.72 | 0.26 | 0.78 | 0.89 | 0.49 | 0.72 | 0.82 | 0.65 | 0.75 | 0.22 | 0.805 | 0.17 | 0.72 | 0.225 | 0.776666667 | 0.176666667 | 0.674 |

| CVD Cancer Diabetes | 0.83 | 0.36 | 0.78 | 0.82 | 0.36 | 0.39 | 1 | 0.9 | 0.805 | 0.345 | 0.825 | 0.33 | 0.61 | 0.325 | 0.68 | 0.316666667 | 0.81 |

| DAC Aid US$ | 0.69 | 0.6 | 0.56 | 0.67 | 0.5 | 0.76 | 0.78 | 0.69 | 0.625 | 0.3 | 0.68 | 0.3 | 0.725 | 0.56 | 0.706666667 | 0.373333333 | 0.558 |

| Days Paid Vacation | 0.44 | 0.21 | 0.64 | 0.57 | 0.5 | 0.55 | 0.64 | 0.5 | 0.54 | 0.205 | 0.505 | 0.23 | 0.495 | 0.355 | 0.52 | 0.32 | 0.55 |

| Death Prob 10-14 | 0.73 | 0.3 | 0.91 | 0.94 | 0.61 | 0.48 | 0.95 | 0.61 | 0.82 | 0.425 | 0.835 | 0.285 | 0.605 | 0.3 | 0.716666667 | 0.29 | 0.742 |

| Death Prob 15-19 | 0.83 | 0.56 | 0.89 | 1 | 0.54 | 0.47 | 1 | 0.71 | 0.86 | 0.67 | 0.915 | 0.445 | 0.65 | 0.43 | 0.766666667 | 0.396666667 | 0.794 |

| Death Prob 20-24 | 0.94 | 0.5 | 0.9 | 0.94 | 0.5 | 0.47 | 0.93 | 1 | 0.92 | 0.545 | 0.94 | 0.415 | 0.705 | 0.4 | 0.783333333 | 0.376666667 | 0.716 |

| Death Prob 5-9 | 0.82 | 0.44 | 0.93 | 0.95 | 0.71 | 0.55 | 1 | 0.73 | 0.875 | 0.22 | 0.885 | 0.22 | 0.685 | 0.37 | 0.773333333 | 0.246666667 | 0.764 |

| Death rate, crude | 0.61 | 0.41 | 0.42 | 0.43 | 0.38 | 0.6 | 0.45 | 0.7 | 0.515 | 0.36 | 0.52 | 0.355 | 0.605 | 0.38 | 0.546666667 | 0.353333333 | 0.496 |

| Death Reporting Infant | 0.61 | 0.42 | 0.67 | 0.74 | 0.4 | 0.56 | 0.64 | 0.69 | 0.64 | 0.48 | 0.675 | 0.375 | 0.585 | 0.37 | 0.636666667 | 0.356666667 | 0.673333333 |

| Death Reporting Total | 0.53 | 0.34 | 0.8 | 0.87 | 0.56 | 0.35 | 0.8 | 0.53 | 0.665 | 0.44 | 0.7 | 0.255 | 0.44 | 0.37 | 0.583333333 | 0.303333333 | 0.733333333 |

| Deaths < 5 | 0.59 | 0.42 | 0.7 | 0.74 | 0.41 | 0.79 | 0.6 | 0.8 | 0.645 | 0.235 | 0.665 | 0.335 | 0.69 | 0.375 | 0.706666667 | 0.333333333 | 0.646 |

| Deaths 10-14 | 0.44 | 0.36 | 0.7 | 0.67 | 0.38 | 0.84 | 0.53 | 0.7 | 0.57 | 0.275 | 0.555 | 0.335 | 0.64 | 0.43 | 0.65 | 0.39 | 0.534 |

| Deaths 15-19 | 0.6 | 0.36 | 0.7 | 0.67 | 0.47 | 0.88 | 0.65 | 0.7 | 0.65 | 0.295 | 0.635 | 0.295 | 0.74 | 0.43 | 0.716666667 | 0.363333333 | 0.622 |

| Deaths 20-24 | 0.47 | 0.32 | 0.7 | 0.67 | 0.35 | 0.83 | 0.59 | 0.6 | 0.585 | 0.29 | 0.57 | 0.265 | 0.65 | 0.36 | 0.656666667 | 0.31 | 0.6 |

| Deaths 5-9 yrs | 0.43 | 0.18 | 0.64 | 0.73 | 0.34 | 0.94 | 0.62 | 0.55 | 0.535 | 0.115 | 0.58 | 0.215 | 0.685 | 0.34 | 0.7 | 0.31 | 0.54 |

| Debt Net Flows Extl | 0.56 | 0 | 0.38 | 0.45 | 0.13 | 0.26 | 0.25 | 0.25 | 0.47 | 0 | 0.505 | 0 | 0.41 | 0 | 0.423333333 | 0 | 0.478 |

| Debt Rescheduled | 0.35 | 0 | 0 | 0 | 0 | 0.35 | 0 | 0.14 | 0.175 | 0 | 0.175 | 0 | 0.35 | 0 | 0.233333333 | 0 | 0.294 |

| Debt Service | 0.26 | 0 | 0.38 | 0.5 | 0.31 | 0.38 | 0.5 | 0.38 | 0.32 | 0 | 0.38 | 0 | 0.32 | 0 | 0.38 | 0 | 0.342 |

| Debt Service | 0.32 | 0 | 0.25 | 0.38 | 0.18 | 0.43 | 0.5 | 0.25 | 0.285 | 0 | 0.35 | 0 | 0.375 | 0 | 0.376666667 | 0 | 0.296 |

| Debt Service | 0.38 | 0 | 0.38 | 0.62 | 0.26 | 0.3 | 0.38 | 0.12 | 0.38 | 0 | 0.5 | 0 | 0.34 | 0 | 0.433333333 | 0 | 0.432 |

| Debt Service | 0.41 | 0 | 0.38 | 0.31 | 0.27 | 0.23 | 0.25 | 0.12 | 0.395 | 0 | 0.36 | 0 | 0.32 | 0 | 0.316666667 | 0 | 0.38 |

| Debt Service | 0.62 | 0 | 0.21 | 0.29 | 0.2 | 0.53 | 0.33 | 0.08 | 0.415 | 0 | 0.455 | 0 | 0.575 | 0 | 0.48 | 0 | 0.336 |

| Debt Service % | 0.26 | 0 | 0.22 | 0.24 | 0.18 | 0.31 | 0.25 | 0.25 | 0.24 | 0 | 0.25 | 0 | 0.285 | 0 | 0.27 | 0 | 0.248 |

| Debt Stock resched | 0.28 | 0 | 0.03 | 0.3 | 0.03 | 0.28 | 0.05 | 0.06 | 0.155 | 0 | 0.29 | 0 | 0.28 | 0 | 0.286666667 | 0 | 0.1525 |

| Democracy Index | 0.86 | 0.36 | 0.86 | 0.8 | 0.65 | 0.36 | 0.92 | 0.92 | 0.86 | 0.325 | 0.83 | 0.295 | 0.61 | 0.295 | 0.673333333 | 0.273333333 | 0.7475 |

| Deposit Int Rate | 0.63 | 0.28 | 0.62 | 0.62 | 0.47 | 0.67 | 0.62 | 0.56 | 0.625 | 0.14 | 0.625 | 0.14 | 0.65 | 0.245 | 0.64 | 0.163333333 | 0.538 |

| Depositors | 0.42 | 0 | 0.54 | 0.54 | 0.27 | 0.41 | 0.55 | 0.4 | 0.48 | 0 | 0.48 | 0 | 0.415 | 0 | 0.456666667 | 0 | 0.49 |

| Depth of Credit Info | 0.24 | 0.21 | 0.33 | 0.34 | 0.34 | 0.46 | 0.29 | 0.16 | 0.285 | 0.28 | 0.29 | 0.195 | 0.35 | 0.255 | 0.346666667 | 0.23 | 0.303333333 |

| Development Asst | 0.74 | 0.4 | 0.78 | 0.76 | 0.25 | 0.72 | 0.78 | 0.69 | 0.76 | 0.2 | 0.75 | 0.2 | 0.73 | 0.46 | 0.74 | 0.306666667 | 0.588 |

| Development Asst | 0.74 | 0.6 | 0.78 | 0.76 | 0.32 | 0.72 | 0.71 | 0.62 | 0.76 | 0.3 | 0.75 | 0.3 | 0.73 | 0.56 | 0.74 | 0.373333333 | 0.576 |

| Disposable Income $US | 0.29 | 0.23 | 0.75 | 0.75 | 0.58 | 0.45 | 0.62 | 1 | 0.52 | 0.26 | 0.52 | 0.19 | 0.37 | 0.26 | 0.496666667 | 0.223333333 | 0.39 |

| Dist.to Frontier | 0.76 | 0.14 | 0.8 | 0.74 | 0.56 | 0.51 | 0.87 | 0.69 | 0.78 | 0.28 | 0.75 | 0.13 | 0.635 | 0.22 | 0.67 | 0.186666667 | 0.766666667 |

| Divorce Rate | 0.21 | 0.13 | 0.49 | 0.57 | 0.5 | 0.3 | 0.57 | 0.32 | 0.35 | 0.18 | 0.39 | 0.18 | 0.255 | 0.265 | 0.36 | 0.253333333 | 0.346 |

| Doctoral | 0.68 | 0.23 | 0.8 | 0.8 | 0.38 | 0.79 | 0.8 | 0.9 | 0.74 | 0.315 | 0.74 | 0.24 | 0.735 | 0.305 | 0.756666667 | 0.286666667 | 0.76 |

| Doctoral Female | 0.84 | 0.23 | 0.76 | 0.8 | 0.43 | 0.67 | 0.84 | 0.9 | 0.8 | 0.305 | 0.82 | 0.215 | 0.755 | 0.305 | 0.77 | 0.27 | 0.8 |

| Doctoral Male | 0.71 | 0.1 | 0.73 | 0.88 | 0.47 | 0.79 | 0.8 | 0.9 | 0.72 | 0.3 | 0.795 | 0.24 | 0.75 | 0.24 | 0.793333333 | 0.286666667 | 0.773333333 |

| Domestic | 0.76 | 0.28 | 0.77 | 0.92 | 0.29 | 0.39 | 0.85 | 0.73 | 0.765 | 0.28 | 0.84 | 0.33 | 0.575 | 0.33 | 0.69 | 0.346666667 | 0.714 |

| Domestic Credit | 0.5 | 0 | 0.41 | 0.53 | 0.25 | 0.31 | 0.58 | 0.5 | 0.455 | 0 | 0.515 | 0 | 0.405 | 0 | 0.446666667 | 0 | 0.442 |

| Domestic Credit LCU | 0.57 | 0.19 | 0.38 | 0.33 | 0.34 | 0.57 | 0.5 | 0.31 | 0.475 | 0.245 | 0.45 | 0.22 | 0.57 | 0.26 | 0.49 | 0.256666667 | 0.396 |

| Domestic Savings %GDP | 0.92 | 0.88 | 0.67 | 0.62 | 0.44 | 0.87 | 0.77 | 0.69 | 0.795 | 0.69 | 0.77 | 0.565 | 0.895 | 0.65 | 0.803333333 | 0.516666667 | 0.63 |

| Domestic Savings LCU | 0.73 | 0.29 | 0.56 | 0.62 | 0.35 | 0.73 | 0.56 | 0.5 | 0.645 | 0.25 | 0.675 | 0.27 | 0.73 | 0.4 | 0.693333333 | 0.35 | 0.582 |

| Domestic Savings US$ | 0.86 | 0.62 | 0.69 | 0.8 | 0.34 | 1 | 0.87 | 0.62 | 0.775 | 0.45 | 0.83 | 0.5 | 0.93 | 0.685 | 0.886666667 | 0.583333333 | 0.736 |

| Drought, flood, temp | 0.51 | 0.28 | 0.75 | 0.68 | 0.5 | 0.63 | 0.69 | 0.71 | 0.63 | 0.39 | 0.595 | 0.265 | 0.57 | 0.29 | 0.606666667 | 0.276666667 | 0.646666667 |

| Ease of Business Index | 0.78 | 0.25 | 0.82 | 0.74 | 0.41 | 0.41 | 0.82 | 0.64 | 0.8 | 0.285 | 0.76 | 0.16 | 0.595 | 0.215 | 0.643333333 | 0.166666667 | 0.78 |

| Econ Fitness | 0.68 | 0.5 | 0.77 | 0.81 | 0.28 | 0.53 | 0.92 | 0.36 | 0.725 | 0.39 | 0.745 | 0.375 | 0.605 | 0.4 | 0.673333333 | 0.35 | 0.753333333 |

| Econ.Dev Assistance | 0.76 | 0.48 | 0.75 | 0.76 | 0.27 | 0.84 | 0.78 | 0.59 | 0.755 | 0.24 | 0.76 | 0.24 | 0.8 | 0.465 | 0.786666667 | 0.31 | 0.572 |

| Economic Freedom | 0.54 | 0.27 | 0.69 | 0.79 | 0.38 | 0.39 | 0.68 | 0.75 | 0.615 | 0.285 | 0.665 | 0.195 | 0.465 | 0.325 | 0.573333333 | 0.256666667 | 0.673333333 |

| Edu Attainment Tertiary F | 0.81 | 0.24 | 0.8 | 0.87 | 0.6 | 0.44 | 0.8 | 0.75 | 0.805 | 0.235 | 0.84 | 0.245 | 0.625 | 0.235 | 0.706666667 | 0.24 | 0.73 |

| Edu Attainment Tertiary M | 0.76 | 0.3 | 0.85 | 0.85 | 0.5 | 0.805 | 0.34 | 0.805 | 0.275 | 0.76 | 0.3 | 0.805 | 0.275 | 0.715 | |||

| Edu Masters Female | 0.58 | 0.16 | 0.85 | 0.92 | 0.55 | 0.73 | 0.79 | 0.82 | 0.715 | 0.28 | 0.75 | 0.27 | 0.655 | 0.33 | 0.743333333 | 0.346666667 | 0.783333333 |

| Edu Masters Male | 0.63 | 0.22 | 0.8 | 0.78 | 0.6 | 0.71 | 0.74 | 0.82 | 0.715 | 0.36 | 0.705 | 0.21 | 0.67 | 0.36 | 0.706666667 | 0.306666667 | 0.736666667 |

| Edu Primary female | 0.69 | 0.35 | 0.8 | 0.73 | 0.57 | 0.59 | 0.75 | 0.67 | 0.745 | 0.505 | 0.71 | 0.255 | 0.64 | 0.34 | 0.67 | 0.28 | 0.63 |

| Edu Secondary | 0.7 | 0.28 | 0.93 | 0.93 | 0.53 | 0.69 | 0.87 | 0.73 | 0.815 | 0.39 | 0.815 | 0.265 | 0.695 | 0.29 | 0.773333333 | 0.276666667 | 0.7225 |

| Edu Spend %GDP | 0.41 | 0.19 | 0.56 | 0.59 | 0.21 | 0.39 | 0.52 | 0.47 | 0.485 | 0.285 | 0.5 | 0.22 | 0.4 | 0.21 | 0.463333333 | 0.223333333 | 0.542 |

| Edu Spend %Gov | 0.46 | 0.13 | 0.52 | 0.52 | 0.44 | 0.24 | 0.43 | 0.29 | 0.49 | 0.13 | 0.49 | 0.19 | 0.35 | 0.18 | 0.406666667 | 0.203333333 | 0.506 |

| Edu Spend/Pupil | 0.63 | 0.11 | 0.67 | 0.69 | 0.32 | 0.49 | 0.8 | 0.73 | 0.65 | 0.265 | 0.66 | 0.18 | 0.56 | 0.305 | 0.603333333 | 0.286666667 | 0.6275 |

| Educ. % of Primary Cmplt | 0.76 | 0.24 | 0.83 | 0.92 | 0.6 | 0.45 | 1 | 0.77 | 0.795 | 0.325 | 0.84 | 0.245 | 0.605 | 0.26 | 0.71 | 0.256666667 | 0.768 |

| Educ. Secondary Pupils | 0.62 | 0.5 | 0.44 | 0.36 | 0.23 | 0.54 | 0.29 | 0.54 | 0.53 | 0.365 | 0.49 | 0.365 | 0.58 | 0.42 | 0.506666667 | 0.356666667 | 0.482 |

| Education Cost | 0.5 | 0 | 0.28 | 0.1 | 0.55 | 0.3 | 0 | 0.18 | 0.39 | 0 | 0.3 | 0 | 0.4 | 0 | 0.3 | 0 | 0.293333333 |

| Education Index | 0.8 | 0.23 | 0.93 | 0.93 | 0.51 | 0.61 | 0.92 | 0.69 | 0.865 | 0.425 | 0.865 | 0.24 | 0.705 | 0.265 | 0.78 | 0.26 | 0.886666667 |

| Education Masters | 0.61 | 0.26 | 0.85 | 0.92 | 0.55 | 0.56 | 0.63 | 0.75 | 0.73 | 0.33 | 0.765 | 0.255 | 0.585 | 0.38 | 0.696666667 | 0.336666667 | 0.793333333 |

| Education Middle | 0.71 | 0.24 | 0.93 | 0.86 | 0.58 | 0.61 | 0.67 | 0.62 | 0.82 | 0.32 | 0.785 | 0.205 | 0.66 | 0.31 | 0.726666667 | 0.263333333 | 0.7075 |

| Education Minimum | 0.59 | 0.28 | 0.86 | 0.86 | 0.53 | 0.51 | 0.71 | 0.71 | 0.725 | 0.205 | 0.725 | 0.265 | 0.55 | 0.255 | 0.653333333 | 0.253333333 | 0.65 |

| Education Pri. Pupils %Fem | 0.69 | 0.54 | 0.75 | 0.88 | 0.41 | 0.53 | 0.69 | 0.69 | 0.72 | 0.48 | 0.785 | 0.42 | 0.61 | 0.55 | 0.7 | 0.466666667 | 0.684 |

| Education to Gr-5 | 0.71 | 0.55 | 0.77 | 0.79 | 0.47 | 0.48 | 1 | 0.77 | 0.74 | 0.535 | 0.75 | 0.4 | 0.595 | 0.42 | 0.66 | 0.363333333 | 0.672 |

| Educational | 0.81 | 0.28 | 0.93 | 0.93 | 0.6 | 0.63 | 0.87 | 0.8 | 0.87 | 0.39 | 0.87 | 0.265 | 0.72 | 0.29 | 0.79 | 0.276666667 | 0.73 |

| Electric Consumptn | 0.82 | 0.53 | 0.92 | 1 | 0.43 | 0.68 | 1 | 0.92 | 0.87 | 0.535 | 0.91 | 0.455 | 0.75 | 0.41 | 0.833333333 | 0.4 | 0.794 |

| Electric Vehicles | 0.38 | 0 | 0 | 0 | 0 | 0.38 | 0 | 0 | 0.19 | 0 | 0.19 | 0 | 0.38 | 0 | 0.253333333 | 0 | 0.126666667 |

| Electric xmit Loss % | 0.69 | 0.29 | 0.81 | 0.85 | 0.43 | 0.32 | 1 | 0.89 | 0.75 | 0.355 | 0.77 | 0.345 | 0.505 | 0.29 | 0.62 | 0.326666667 | 0.67 |

| Electricity Access %Pop | 0.44 | 0 | 0.52 | 0.64 | 0.31 | 0.47 | 0.5 | 0.48 | 0.48 | 0 | 0.54 | 0 | 0.455 | 0.21 | 0.516666667 | 0.14 | 0.604 |

| Emission Damage | 0.9 | 0.27 | 1 | 1 | 0.6 | 0.51 | 1 | 1 | 0.95 | 0.435 | 0.95 | 0.235 | 0.705 | 0.385 | 0.803333333 | 0.323333333 | 0.89 |

| Empl Agri Female | 0.83 | 0.6 | 0.76 | 0.94 | 0.4 | 0.74 | 0.9 | 0.9 | 0.795 | 0.56 | 0.885 | 0.45 | 0.785 | 0.51 | 0.836666667 | 0.44 | 0.72 |

| Empl Agri Male % | 0.8 | 0.38 | 0.94 | 1 | 0.41 | 0.65 | 0.94 | 0.94 | 0.87 | 0.54 | 0.9 | 0.39 | 0.725 | 0.44 | 0.816666667 | 0.426666667 | 0.798 |

| Empl Agriculture | 0.9 | 0.6 | 0.88 | 1 | 0.41 | 0.6 | 0.94 | 1 | 0.89 | 0.65 | 0.95 | 0.5 | 0.75 | 0.55 | 0.833333333 | 0.5 | 0.794 |

| Empl.Services %Fem | 0.79 | 0.32 | 0.77 | 0.92 | 0.33 | 0.43 | 0.85 | 1 | 0.78 | 0.3 | 0.855 | 0.275 | 0.61 | 0.32 | 0.713333333 | 0.29 | 0.68 |

| Empl:Pop Ratio 15-24 | 0.49 | 0.21 | 0.24 | 0.25 | 0.28 | 0.24 | 0.38 | 0.38 | 0.365 | 0.295 | 0.37 | 0.26 | 0.365 | 0.265 | 0.326666667 | 0.28 | 0.366 |

| Empl:Pop Ratio Female | 0.45 | 0.28 | 0.6 | 0.54 | 0.34 | 0.39 | 0.67 | 0.62 | 0.525 | 0.28 | 0.495 | 0.225 | 0.42 | 0.3 | 0.46 | 0.256666667 | 0.544 |

| Empl:Pop Ratio Male | 0.46 | 0.62 | 0.6 | 0.63 | 0.56 | 0.41 | 0.53 | 0.53 | 0.53 | 0.405 | 0.545 | 0.465 | 0.435 | 0.59 | 0.5 | 0.496666667 | 0.54 |

| Empl:Population Ratio | 0.56 | 0.5 | 0.47 | 0.41 | 0.38 | 0.35 | 0.35 | 0.63 | 0.515 | 0.38 | 0.485 | 0.405 | 0.455 | 0.49 | 0.44 | 0.43 | 0.408 |

| Emplmt Compensation | 0.37 | 0.09 | 0.56 | 0.53 | 0.4 | 0.27 | 0.44 | 0.47 | 0.465 | 0.165 | 0.45 | 0.17 | 0.32 | 0.165 | 0.39 | 0.193333333 | 0.422 |

| Emplmt Compensation | 0.68 | 0.36 | 0.78 | 0.67 | 0.56 | 0.5 | 0.71 | 0.6 | 0.73 | 0.405 | 0.675 | 0.315 | 0.59 | 0.28 | 0.616666667 | 0.276666667 | 0.64 |

| Emplmt Services %Male | 0.71 | 0.32 | 0.8 | 1 | 0.36 | 0.49 | 0.85 | 0.92 | 0.755 | 0.43 | 0.855 | 0.315 | 0.6 | 0.32 | 0.733333333 | 0.316666667 | 0.64 |

| Employers Female | 0.55 | 0.42 | 0.46 | 0.52 | 0.44 | 0.61 | 0.56 | 0.4 | 0.505 | 0.3 | 0.535 | 0.335 | 0.58 | 0.37 | 0.56 | 0.33 | 0.482 |

| Employment | 0.45 | 0.5 | 0.48 | 0.49 | 0.29 | 0.39 | 0.55 | 0.44 | 0.465 | 0.4 | 0.47 | 0.405 | 0.42 | 0.41 | 0.443333333 | 0.376666667 | 0.512 |

| Employment | 0.61 | 0.33 | 0.85 | 0.92 | 0.5 | 0.46 | 1 | 1 | 0.73 | 0.355 | 0.765 | 0.32 | 0.535 | 0.365 | 0.663333333 | 0.346666667 | 0.64 |

| Energy Depltn | 0.66 | 0.44 | 0.55 | 0.57 | 0.42 | 0.59 | 0.32 | 0.47 | 0.605 | 0.385 | 0.615 | 0.385 | 0.625 | 0.42 | 0.606666667 | 0.39 | 0.58 |

| Energy Imports % | 0.65 | 0.27 | 0.3 | 0.42 | 0.4 | 0.6 | 0.42 | 0.28 | 0.475 | 0.225 | 0.535 | 0.235 | 0.625 | 0.325 | 0.556666667 | 0.283333333 | 0.516 |

| Energy Intensity Level | 0.67 | 0.19 | 0.37 | 0.56 | 0.23 | 0.48 | 0.34 | 0.43 | 0.52 | 0.235 | 0.615 | 0.21 | 0.575 | 0.21 | 0.57 | 0.216666667 | 0.45 |

| Energy Methane | 0.48 | 0.6 | 0.47 | 0.61 | 0.2 | 0.88 | 0.54 | 0.47 | 0.475 | 0.45 | 0.545 | 0.455 | 0.68 | 0.625 | 0.656666667 | 0.52 | 0.516 |

| Energy Methane | 0.69 | 0.62 | 0.65 | 0.57 | 0.24 | 0.61 | 0.5 | 0.79 | 0.67 | 0.375 | 0.63 | 0.37 | 0.65 | 0.575 | 0.623333333 | 0.423333333 | 0.572 |

| Energy Use | 0.32 | 0.23 | 0.27 | 0.4 | 0.24 | 0.51 | 0.21 | 0.27 | 0.295 | 0.315 | 0.36 | 0.265 | 0.415 | 0.325 | 0.41 | 0.316666667 | 0.376 |

| Energy Use | 0.42 | 0.16 | 0.3 | 0.61 | 0.4 | 0.59 | 0.34 | 0.32 | 0.36 | 0.22 | 0.515 | 0.23 | 0.505 | 0.29 | 0.54 | 0.293333333 | 0.458 |

| Energy Use | 0.83 | 0.3 | 1 | 0.92 | 0.5 | 0.52 | 0.93 | 1 | 0.915 | 0.485 | 0.875 | 0.34 | 0.675 | 0.3 | 0.756666667 | 0.326666667 | 0.806 |

| Energy Use Kg Oil | 0.36 | 0.21 | 0.31 | 0.46 | 0.21 | 0.51 | 0.27 | 0.13 | 0.335 | 0.255 | 0.41 | 0.22 | 0.435 | 0.255 | 0.443333333 | 0.246666667 | 0.394 |

| Equity Inflows $US | 0.68 | 0.45 | 0.74 | 0.78 | 0.58 | 0.69 | 0.89 | 0.75 | 0.71 | 0.385 | 0.73 | 0.31 | 0.685 | 0.45 | 0.716666667 | 0.356666667 | 0.722 |

| Errors & Omissions | 0.53 | 0.39 | 0.74 | 0.84 | 0.37 | 0.69 | 0.9 | 0.7 | 0.635 | 0.36 | 0.685 | 0.32 | 0.61 | 0.325 | 0.686666667 | 0.3 | 0.738 |

| Exchange Index | 0.52 | 0.28 | 0.57 | 0.39 | 0.46 | 0.39 | 0.57 | 0.45 | 0.545 | 0.28 | 0.455 | 0.265 | 0.455 | 0.39 | 0.433333333 | 0.343333333 | 0.474 |

| Expenditure | 0.63 | 0.4 | 0.47 | 0.51 | 0.53 | 0.49 | 0.57 | 0.38 | 0.55 | 0.345 | 0.57 | 0.24 | 0.56 | 0.47 | 0.543333333 | 0.34 | 0.526 |

| Export cost, Doc Complce | 0.62 | 0.29 | 0.8 | 0.88 | 0.58 | 0.59 | 0.82 | 0.55 | 0.71 | 0.315 | 0.75 | 0.295 | 0.605 | 0.29 | 0.696666667 | 0.293333333 | 0.766666667 |

| Export G & S | 0.82 | 0.62 | 0.8 | 0.87 | 0.5 | 1 | 0.85 | 0.69 | 0.81 | 0.5 | 0.845 | 0.435 | 0.91 | 0.685 | 0.896666667 | 0.54 | 0.8 |

| Export High Incomes | 0.48 | 0.32 | 0.61 | 0.63 | 0.5 | 0.56 | 0.67 | 0.62 | 0.545 | 0.41 | 0.555 | 0.285 | 0.52 | 0.4 | 0.556666667 | 0.35 | 0.566 |

| Export Lead time | 0.47 | 0.17 | 0.5 | 0.47 | 0.25 | 0.37 | 0.42 | 0.43 | 0.485 | 0.25 | 0.47 | 0.125 | 0.42 | 0.275 | 0.436666667 | 0.21 | 0.47 |

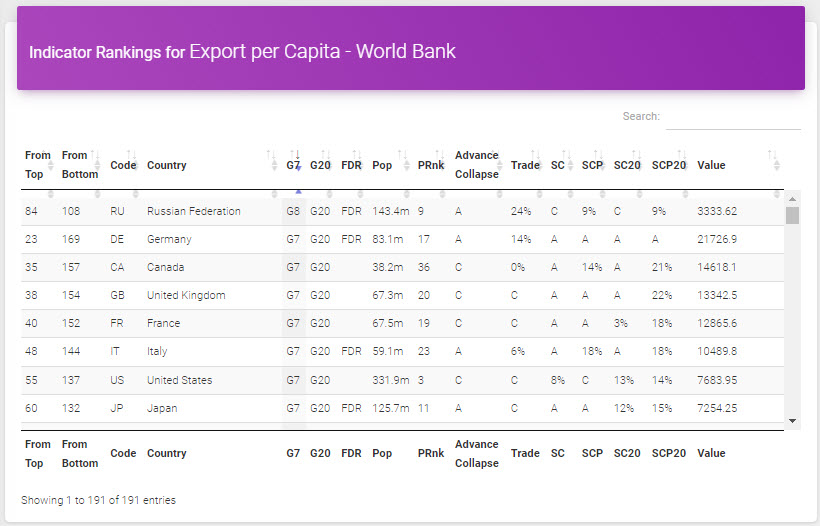

| Export per Capita | 1 | 0.62 | 0.93 | 0.93 | 0.71 | 0.67 | 1 | 0.85 | 0.965 | 0.58 | 0.965 | 0.345 | 0.835 | 0.475 | 0.866666667 | 0.34 | 0.96 |

| Export Value Index | 0.36 | 0.32 | 0.49 | 0.4 | 0.31 | 0.43 | 0.41 | 0.53 | 0.425 | 0.36 | 0.38 | 0.26 | 0.395 | 0.365 | 0.396666667 | 0.31 | 0.444 |

| Export Volume Index | 0.45 | 0.5 | 0.38 | 0.5 | 0.31 | 0.56 | 0.41 | 0.47 | 0.415 | 0.415 | 0.475 | 0.35 | 0.505 | 0.455 | 0.503333333 | 0.37 | 0.456 |

| Exports $US | 0.87 | 0.8 | 0.73 | 0.85 | 0.5 | 1 | 0.85 | 0.77 | 0.8 | 0.55 | 0.86 | 0.525 | 0.935 | 0.775 | 0.906666667 | 0.6 | 0.792 |

| Exports %GDP | 0.92 | 0.5 | 0.62 | 0.51 | 0.44 | 0.39 | 0.52 | 0.62 | 0.77 | 0.4 | 0.715 | 0.31 | 0.655 | 0.425 | 0.606666667 | 0.323333333 | 0.598 |

| Exports %Growth | 0.57 | 0.23 | 0.49 | 0.48 | 0.47 | 0.38 | 0.49 | 0.43 | 0.53 | 0.23 | 0.525 | 0.15 | 0.475 | 0.265 | 0.476666667 | 0.2 | 0.54 |

| Exports 2010 US$ | 0.82 | 0.62 | 0.73 | 0.83 | 0.5 | 1 | 0.85 | 0.69 | 0.775 | 0.46 | 0.825 | 0.435 | 0.91 | 0.62 | 0.883333333 | 0.496666667 | 0.806 |

| Exports BoP$ | 0.77 | 0.75 | 0.8 | 0.92 | 0.44 | 1 | 0.92 | 0.85 | 0.785 | 0.565 | 0.845 | 0.5 | 0.885 | 0.75 | 0.896666667 | 0.583333333 | 0.798 |

| Exports capcty to Import | 0.65 | 0.67 | 0.46 | 0.53 | 0.4 | 0.52 | 0.5 | 0.47 | 0.555 | 0.545 | 0.59 | 0.46 | 0.585 | 0.605 | 0.566666667 | 0.486666667 | 0.504 |

| Exports C-LCU | 0.71 | 0.67 | 0.43 | 0.46 | 0.4 | 0.46 | 0.5 | 0.47 | 0.57 | 0.545 | 0.585 | 0.46 | 0.585 | 0.605 | 0.543333333 | 0.486666667 | 0.51 |

| Exports ICT %Ex | 0.31 | 0.35 | 0.38 | 0.51 | 0.53 | 0.26 | 0.28 | 0.41 | 0.345 | 0.325 | 0.41 | 0.3 | 0.285 | 0.41 | 0.36 | 0.356666667 | 0.43 |

| Exports ICT US$ | 0.65 | 0.42 | 0.86 | 0.92 | 0.41 | 0.76 | 0.92 | 0.79 | 0.755 | 0.42 | 0.785 | 0.335 | 0.705 | 0.355 | 0.776666667 | 0.32 | 0.708 |

| Exports LCU | 0.69 | 0.54 | 0.4 | 0.49 | 0.24 | 0.39 | 0.5 | 0.56 | 0.545 | 0.48 | 0.59 | 0.395 | 0.54 | 0.53 | 0.523333333 | 0.436666667 | 0.47 |

| Exports Merch $US | 0.72 | 0.42 | 0.77 | 0.75 | 0.5 | 0.94 | 0.85 | 0.56 | 0.745 | 0.35 | 0.735 | 0.335 | 0.83 | 0.5 | 0.803333333 | 0.416666667 | 0.734 |

| Exports Service | 0.72 | 0.47 | 0.87 | 0.87 | 0.4 | 0.71 | 0.92 | 0.85 | 0.795 | 0.425 | 0.795 | 0.36 | 0.715 | 0.37 | 0.766666667 | 0.33 | 0.804 |

| Exports to LI | 0.5 | 0.25 | 0.44 | 0.43 | 0.47 | 0.67 | 0.6 | 0.44 | 0.47 | 0.275 | 0.465 | 0.315 | 0.585 | 0.26 | 0.533333333 | 0.3 | 0.496 |

| Exports to low mid MidEast | 0.55 | 0.42 | 0.56 | 0.62 | 0.53 | 0.37 | 0.56 | 0.5 | 0.555 | 0.37 | 0.585 | 0.27 | 0.46 | 0.48 | 0.513333333 | 0.36 | 0.458 |

| Exports Transport Service | 0.36 | 0.24 | 0.43 | 0.48 | 0.38 | 0.36 | 0.34 | 0.43 | 0.395 | 0.33 | 0.42 | 0.22 | 0.36 | 0.31 | 0.4 | 0.273333333 | 0.38 |

| Exports Travel Services | 0.52 | 0.38 | 0.69 | 0.61 | 0.53 | 0.38 | 0.6 | 0.43 | 0.605 | 0.255 | 0.565 | 0.315 | 0.45 | 0.345 | 0.503333333 | 0.313333333 | 0.552 |

| Ext Debt Stocks | 0.44 | 0 | 0.29 | 0.36 | 0.18 | 0.44 | 0.25 | 0.25 | 0.365 | 0 | 0.4 | 0 | 0.44 | 0 | 0.413333333 | 0 | 0.398 |

| Ext Debt Stocks | 0.54 | 0 | 0.23 | 0.24 | 0.15 | 0.32 | 0.42 | 0.12 | 0.385 | 0 | 0.39 | 0 | 0.43 | 0 | 0.366666667 | 0 | 0.382 |

| Ext Debt Stocks | 0.54 | 0 | 0.31 | 0.38 | 0.38 | 0.4 | 0.33 | 0.07 | 0.425 | 0 | 0.46 | 0 | 0.47 | 0 | 0.44 | 0 | 0.43 |

| Ext Debt Stocks | 0.55 | 0 | 0.3 | 0.31 | 0.23 | 0.39 | 0.5 | 0.21 | 0.425 | 0 | 0.43 | 0 | 0.47 | 0 | 0.416666667 | 0 | 0.412 |

| Ext. Debt % Exports | 0.38 | 0 | 0.27 | 0.41 | 0.33 | 0.46 | 0.33 | 0.15 | 0.325 | 0 | 0.395 | 0 | 0.42 | 0 | 0.416666667 | 0 | 0.353333333 |

| Ext. Debt %GNI | 0.42 | 0 | 0.38 | 0.43 | 0.38 | 0.37 | 0.62 | 0.38 | 0.4 | 0 | 0.425 | 0 | 0.395 | 0 | 0.406666667 | 0 | 0.41 |

| Ext. Debt US$ | 0.44 | 0 | 0.29 | 0.36 | 0.16 | 0.38 | 0.25 | 0.13 | 0.365 | 0 | 0.4 | 0 | 0.41 | 0 | 0.393333333 | 0 | 0.363333333 |

| External Debt Creditors | 0.32 | 0 | 0.5 | 0.5 | 0.25 | 0.56 | 0.62 | 0.44 | 0.41 | 0 | 0.41 | 0 | 0.44 | 0 | 0.46 | 0 | 0.472 |

| External Debt Private | 0.27 | 0 | 0.22 | 0.44 | 0.3 | 0.5 | 0.3 | 0.12 | 0.245 | 0 | 0.355 | 0 | 0.385 | 0 | 0.403333333 | 0 | 0.36 |

| External Debt Total | 0.32 | 0 | 0.62 | 0.62 | 0.31 | 0.67 | 0.62 | 0.44 | 0.47 | 0 | 0.47 | 0 | 0.495 | 0 | 0.536666667 | 0 | 0.508 |

| Family Workers | 0.74 | 0.34 | 0.9 | 0.9 | 0.47 | 0.78 | 0.9 | 0.88 | 0.82 | 0.32 | 0.82 | 0.295 | 0.76 | 0.38 | 0.806666667 | 0.336666667 | 0.78 |

| FDI In (US$) | 0.65 | 0.5 | 0.7 | 0.85 | 0.7 | 0.71 | 0.8 | 0.63 | 0.675 | 0.48 | 0.75 | 0.405 | 0.68 | 0.48 | 0.736666667 | 0.423333333 | 0.73 |

| FDI Inflows %GDP | 0.42 | 0.28 | 0.52 | 0.46 | 0.54 | 0.37 | 0.48 | 0.48 | 0.47 | 0.305 | 0.44 | 0.265 | 0.395 | 0.215 | 0.416666667 | 0.226666667 | 0.464 |

| FDI Net Out | 0.8 | 0.49 | 0.77 | 0.81 | 0.38 | 0.76 | 0.92 | 0.77 | 0.785 | 0.395 | 0.805 | 0.37 | 0.78 | 0.49 | 0.79 | 0.41 | 0.794 |

| FDI Net US$ | 0.81 | 0.29 | 1 | 0.94 | 0.37 | 0.82 | 0.92 | 0.85 | 0.905 | 0.355 | 0.875 | 0.23 | 0.815 | 0.29 | 0.856666667 | 0.25 | 0.852 |

| FDI Outflows % GDP | 0.74 | 0.5 | 0.68 | 0.7 | 0.3 | 0.37 | 0.85 | 0.73 | 0.71 | 0.32 | 0.72 | 0.375 | 0.555 | 0.355 | 0.603333333 | 0.32 | 0.698 |

| Fed Gov Debt | 0.39 | 0.38 | 0.43 | 0.52 | 0.36 | 0.32 | 0.54 | 0.47 | 0.41 | 0.335 | 0.455 | 0.27 | 0.355 | 0.38 | 0.41 | 0.306666667 | 0.334 |

| Fem Married at 18 | 0.39 | 0 | 0.38 | 0.75 | 0.33 | 0.3 | 0.27 | 0.5 | 0.385 | 0 | 0.57 | 0 | 0.345 | 0 | 0.48 | 0 | 0.4625 |

| Female %Pop 25-29 | 0.48 | 0.24 | 0.8 | 0.78 | 0.35 | 0.43 | 0.84 | 0.7 | 0.64 | 0.195 | 0.63 | 0.205 | 0.455 | 0.325 | 0.563333333 | 0.273333333 | 0.686 |

| Female %Pop 55-59 | 0.62 | 0.31 | 0.73 | 0.93 | 0.47 | 0.68 | 0.81 | 0.62 | 0.675 | 0.305 | 0.775 | 0.305 | 0.65 | 0.395 | 0.743333333 | 0.363333333 | 0.682 |

| Female Headed Hsehlds | 0.36 | 0 | 0.15 | 0.25 | 0.3 | 0.36 | 0.25 | 0.08 | 0.255 | 0 | 0.305 | 0 | 0.36 | 0 | 0.323333333 | 0 | 0.253333333 |

| Female Mutilation | 0.03 | 0 | 0 | 0 | 0 | 0.03 | 0 | 0.09 | 0.015 | 0 | 0.015 | 0 | 0.03 | 0 | 0.02 | 0 | 0.01 |

| Female Top Mgr | 0.39 | 0 | 0.33 | 0.38 | 0.22 | 0.36 | 0.26 | 0.29 | 0.36 | 0 | 0.385 | 0 | 0.375 | 0 | 0.376666667 | 0 | 0.3575 |

| Females Out of School | 0.66 | 0.25 | 0.71 | 0.76 | 0.44 | 0.59 | 0.67 | 0.71 | 0.685 | 0.27 | 0.71 | 0.315 | 0.625 | 0.375 | 0.67 | 0.376666667 | 0.594 |

| Fertility Age 15-19 | 0.78 | 0.55 | 0.9 | 0.94 | 0.6 | 0.57 | 1 | 1 | 0.84 | 0.465 | 0.86 | 0.375 | 0.675 | 0.48 | 0.763333333 | 0.386666667 | 0.788 |

| Fertility Rate | 0.68 | 0.5 | 0.82 | 0.82 | 0.47 | 0.49 | 0.76 | 0.6 | 0.75 | 0.36 | 0.75 | 0.305 | 0.585 | 0.5 | 0.663333333 | 0.37 | 0.724 |

| Fertilizer Consumption | 0.67 | 0.42 | 0.46 | 0.47 | 0.31 | 0.24 | 0.42 | 0.81 | 0.565 | 0.285 | 0.57 | 0.3 | 0.455 | 0.285 | 0.46 | 0.25 | 0.532 |

| Fertilizer per Acre | 0.64 | 0.21 | 0.73 | 0.75 | 0.36 | 0.33 | 0.49 | 0.44 | 0.685 | 0.21 | 0.695 | 0.23 | 0.485 | 0.255 | 0.573333333 | 0.253333333 | 0.614 |

| Final | 0.55 | 0.23 | 0.59 | 0.6 | 0.32 | 0.35 | 0.57 | 0.6 | 0.57 | 0.22 | 0.575 | 0.24 | 0.45 | 0.275 | 0.5 | 0.266666667 | 0.536 |

| Financial Account US$ | 0.89 | 0.75 | 0.92 | 0.85 | 0.31 | 0.87 | 0.85 | 0.77 | 0.905 | 0.515 | 0.87 | 0.46 | 0.88 | 0.645 | 0.87 | 0.486666667 | 0.886 |

| Financials % Export | 0.45 | 0.43 | 0.4 | 0.33 | 0.44 | 0.48 | 0.53 | 0.56 | 0.425 | 0.325 | 0.39 | 0.34 | 0.465 | 0.265 | 0.42 | 0.26 | 0.402 |

| Fish Threatened | 0.25 | 0.44 | 0.65 | 0.59 | 0.5 | 0.42 | 0.39 | 0.41 | 0.45 | 0.385 | 0.42 | 0.345 | 0.335 | 0.48 | 0.42 | 0.403333333 | 0.496666667 |

| Fixed Broadband | 0.81 | 0.32 | 0.92 | 1 | 0.57 | 0.52 | 1 | 0.85 | 0.865 | 0.41 | 0.905 | 0.285 | 0.665 | 0.32 | 0.776666667 | 0.296666667 | 0.81 |

| Fixed Phones | 0.65 | 0.28 | 0.85 | 0.92 | 0.43 | 0.54 | 0.92 | 0.8 | 0.75 | 0.255 | 0.785 | 0.265 | 0.595 | 0.315 | 0.703333333 | 0.293333333 | 0.758 |

| Fixed Phones | 0.67 | 0.42 | 0.67 | 0.77 | 0.38 | 0.65 | 0.73 | 0.54 | 0.67 | 0.325 | 0.72 | 0.335 | 0.66 | 0.35 | 0.696666667 | 0.316666667 | 0.674 |

| Food | 0.5 | 0.3 | 0.76 | 0.76 | 0.29 | 0.26 | 0.65 | 0.53 | 0.63 | 0.31 | 0.63 | 0.3 | 0.38 | 0.365 | 0.506666667 | 0.343333333 | 0.636 |

| Food | 0.81 | 0.45 | 0.76 | 0.81 | 0.53 | 0.54 | 0.88 | 0.76 | 0.785 | 0.385 | 0.81 | 0.35 | 0.675 | 0.375 | 0.72 | 0.333333333 | 0.746 |