- This topic has 0 replies, 1 voice, and was last updated 9 years, 1 month ago by

etilley.

-

AuthorPosts

-

June 14, 2017 at 10:22 am #6612

etilley

Keymaster

Canada’s Finance Industry is failing our Economy

In Two-Parts

Part 1

Large Financial Institutions are faced with the challenge of investing our pensions and investments wisely on a daily and monthly basis in Canada. Investors want performance; pensioners want retirement incomes that are protected from Inflation; and for these reasons, we all want to manage Risk well. Risk is the term given to the chance that your investment won’t be returned in its entirety – when you need it.

Obviously no-one wants to lose their investment, but making your money work for you makes a lot of sense too. Inflation adds risk to your savings when you do nothing with your money, and this means that a zero-risk plan is not smart either.

In Canada, unfortunately, we can add “Open” government policy to our list of Inflation and Economic problems. Policy shortcomings in Canada permitted 13-times increases in housing bubbles, they more than doubled energy costs within the last five or eight years, and created fairly-unprecedented cost-of-living inflation increases; increases – that were prevented by better-management teams in other countries like the Netherlands.

A low-risk investment is strongly assured; a high-risk investment can be quite a bit less so; neither – is absolutely guaranteed but in a stable financial setting, low-risk investments within known low-risk institutions – offer safe-small returns. High-risk investments offer less assurance, but offset this risk by promising higher returns. Truly it’s a wonder that it works at all, but like magnetic blips on your computer’s hard-drive, the systems work reliably enough.

In World Peace – the Transition, I discussed a thought-leadership approach that looked at topics from three viewpoints: from the detailed views of a forest’s blades of grass, to a 100,000 foot view of the entire forest, and then I suggested that a view from space was important.

The Highest Point-of-View; the International Overview

From the vantage of a spacecraft, one can see the earth without the little lines that separate countries on a map; indeed the notion of countries doesn’t appear to make a lot of sense from this viewpoint. Clearly the entire globe is just one big floating ball in space after all. Surely the needs of people on the left side of the planet don’t differ greatly from the folks on the right?

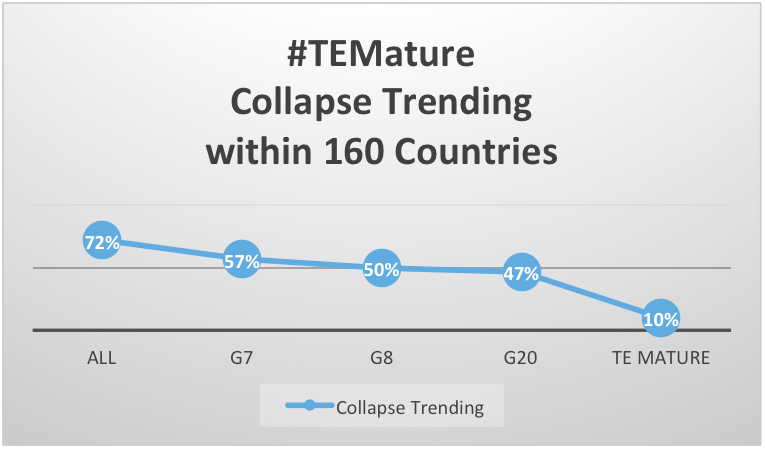

How are their financial institutions doing from up here at this level ? Click on the picture for a deeper explanation of these readily-collected GDP statistics.

Ok – well from this vantage, clearly there is room for improvement. 72% of all countries surveyed; and 60% of the G7 are in a collapse-trending. This means that our countries spend more than they earn and they have been doing that for a long enough time to have amassed more than their Annual GDPs in Debt as well. This chart doesn’t talk about Rate of Collapse nor how far along is the Collapse; this just indicates that 72% of all national economies are on their way.

Financial Sectors provide for themselves well-enough across the board with few known exceptions, so there is no obvious correlation between a Healthy Financial Sector and a strong Economy.

Is a Financial Industry necessary? I think everyone can agree that the answer is Yes – we currently live within a global monetary system and our community will have need of money right up until all of our needs of food, housing, transport, and so on – are automated without charge. Won’t that be nice? Yes – of course it will – and you can read about how to take the pain out of transitioning to a Good Life within an automated community here.

Is there an inverse correlation too; do healthy Finance Sectors actually create weak Economies? Very often, the empirically proven answer is Yes. Before we get to the empirical stats, look at this question intuitively: If GDPs are influenced by financial institutions in a statistically-significant way – and I think that most of us imagine that this is a true statement, then the consistently-strong Financial Sectors of the world do in fact, create unhealthy Economies 72% of the time (according to the chart above).

Major studies have concluded that the size of a Financial Sector is definitely a factor. As Finance Sector salaries reach 80% to 100% of a GDP, that large finance community will cause an economy to suffer consistently – https://link.springer.com/article/10.1007/s10663-016-9323-9.

Mature, FinTech-enabled banking automations emulate larger size and efficiency too – and so a mature Finance Industry, such as the financial institutions of Canada, can be counted among this detrimental group fairly – I think.

What about all of the Economists that have graduated from our very expensive universities this past 100-years? Surely they are responsible for maintaining a sustainable economy. While it’s true that not all of these grads have jobs with the financial industry and can, therefore, speak candidly about prudent next steps without conflict-of-interest. They should be able to protect us – yes?

No – not at all – for a few reasons. For starters, more Economists work with the Private Sector because Government Jobs pay much less. Salaries are just $57,000 in the U.S. – versus $200k+ in Private Financial placements.

Economics Faculties, too, have failed to insist on rigour in Scientific Method & Observation too; preferring instead, a much more theoretical Peer-Reviewed curriculum this past many years. If you took an economics course in University, you probably know much about proven-inaccurate Keynes Theory – but you likely learned little or nothing about empirically-validatable Schumpeter, Kondratiev, and Thompson.

In my book Transition Economics – The Science of Sustainable Economies, I discuss how this inexplicable bias has introduced Economics students to an almost completely unscientific Economics curriculum for many decades now.

Because the U.S. employed Keynesian method for many years (enabling it to run full force into an economic wall in 2008 – I might add), it actually become career-jeopardizing for an Economist to speak of empirically-proven capitalism mitigations that could be proven in scientific method and observation. It was unacceptable – both politically and academically; I envision being called a Liberal or a Communist because I wasn’t playing by the American Capitalist rule-book. Worse, you simply could not count on completing a degree reliably without adhering to rote.

Because the U.S. employed Keynesian method for many years (enabling it to run full force into an economic wall in 2008 – I might add), it actually become career-jeopardizing for an Economist to speak of empirically-proven capitalism mitigations that could be proven in scientific method and observation. It was unacceptable – both politically and academically; I envision being called a Liberal or a Communist because I wasn’t playing by the American Capitalist rule-book. Worse, you simply could not count on completing a degree reliably without adhering to rote.Science, however, doesn’t care if it’s socially acceptable when it proves that Capitalist policies are predictably unsustainable – and also probably led to World Wars I and II before continuing on to give us our present-day global Great Depression.

Philosophy 101 – Fear of nature is nonsensical. Socrates put it: Great Philosophy is great Leadership.

Some capitalist policies are plainly inappropriate at some points within 3500-year-recorded 60-year Capitalist cycles; there is nothing fearful about this reality. We know what’s coming and we make adjustments to our policies – or we permit all hell to break loose when we don’t. Simple.

Every country’s policies have only ever been a blend of communist, socialist, and capitalist policies throughout history. If you don’t realize that every country runs Communist Policy, widen your learning. Getting the blend of policies correct for the times – is the most important thing we can do as a nation.

A Good Life must be maintained or financial and democratic collapse are certain. I like JFK’s words best:

Those who make peaceful revolution impossible; make violent revolution inevitable

The 100,000 foot view – “The Forest”

Let’s take a look at how individual countries either kept their economies advancing, or began to collapse them…

China proved itself an excellent Economic Planner when it began monetizing its Economy 30-years ago. To do this, it balanced capitalistic policies that supported its trade-incomes, alongside communistic policies which worked toward self-sufficiency. Brilliant. It didn’t shrink in fear of Capitalistic Policy; as the Americans surely did of Socialistic Policy.

The Netherlands, and other small population countries like Norway and Denmark, quickly saw that their economies and livelihoods were damaged once the 1980’s “Greed is Good” Open Model was tried in the booming Capitalism of the 1980s, so they turned instead to Socialistic sustainable policies that protected their “Good Lives”. Most of these countries continue to live the American Dream today – with Advancing Economies as well.

Canada, on the other hand, embraced its “famously Open Policies”; Justin Trudeau was on the news saying these words just a week ago. Yes, of course Canada is Collapsing-Trending. “Open Policies” are the words of a political marketing engine that little-understands what it takes to build a “Right Plan” – Aristotle’s term for the Strategic Plan for Sustainable Communities and Economies. See Politic 322 BC. translation by Messerly.

Canadian politicians – like their US counterparts, let the private financial sector take care of themselves. Not surprisingly, that private sector took excellent care – of themselves. The banks do throw a few charitable events now and again – but are generally painted negatively by young MBA grads and society alike. If this continues, what comes next is demonstrations; and history teaches us that revolution/populist fires start to blaze; as rioters already protest in Britain, the US, Greece, Spain, Venezuela, and so forth.

Financial Decisions/Policies that benefit fund owners, but lead the host economy to collapse, are unsustainable.

The Need of Government Policy in Finance

Large Financial Sectors damage economies; we’ve chatted about this. The degree to which Finance Sectors detriment any country’s economy must be discussed alongside the government policy that manages the financial institution – as follows:

Are Financial Institutions:

- paying tax?

- are they hiring locally?

- are they investing in projects that directly benefit Canadian Self-sufficiency and Exports (Economic Targets needed to build a strong economy)

- are they preventing usury? Mortgages that will never be repaid.

Let’s see, in Canada – Mostly No, partly No, er-um – No – to that third question too; and the Economy has been collapsing at an accelerating rate since 2008. Ok, so have we had enough with the “Open Policies” yet?

Part 2

The View from “the Trees” Detail Level

This is the level of detail that is needed to understand our failed supports for Innovation, OnShoring, Interest Rates, Mortgage Usury and other major issues in Canada.

When economies are flourishing, there is little need to revise status-quo processes; but when you’re heading for a cliff, status quo doesn’t help and neither does slowing the status-quo. You need a proven 180-degree turn.

How does Unsustainable Financial Policy impact “the trees and the blades-of-grass” detail viewpoint of Canada’s Economy? Our Economic Collapse-trendings have impacted millions and millions of individuals already. Read about these impacts on Canada’s Population here; and to keep our story on track, let us now discuss specifically how does the financial industry keep us headed in this collapsing trajectory – and how can we turn it around?

There are problems in many areas of Government Policy in regards of Finance – in Innovation, in Corporate Tax Evasion, in Offshoring Engineering, and so on – so let’s examine one problem as an example of how we can approach others similarly.

Failing at Innovation

How did our “Open” Financial Policies impact Innovation in Canada?

Innovation is impacting the Economy directly right now, as many jobs are being automated, or offshored through communication technology advances. And we haven’t seen anything yet.

Consider that within five years, Canada will be competing directly with trade from mature, automated production lines in Germany, China, and other nations – which can turn off their shop-floor lights and create better products more cheaply. They – will improve trade revenues as they sleep; we – will become reliant on imports that we cannot pay for due to the shortfall in our export trade revenues.

In a global monetary system, every country must monetize (through export) and also build self-sustainability (that reduce imports) or it will collapse. Canada’s will resemble the economy of 1986 USSR, if it cannot sustain a trade-surplus that can assist eliminating our considerable debt; and the U.S. and the U.K. can say the same.

Innovation is a critical Economic Injector, just like purchasing Foreign Debt, or any other. Income Support Policies would allow us to adopt automation quickly without injury to families, and I have discussed previously here how these same supports can create an additional $630 billion dollars in annual exports for Canada when managed well.

Yet, in the past ten-years, Canada has created no multi-billion-dollar hi-techs; no Airbnb, no Zillow, no Salesforce, no Google, no nothing at all – nada – squat – zip. That’s a fact – and you can safely ignore the FinTech flash-in-pan creations of our investment bankers this year – for the reasons mentioned above too.

Accelerators – Failed Innovation

Over the last ten-year period we have funded accelerators like MARs, Communitech, and a network of business call centers across the country offering “counseling and advice”. Clearly, the programs offered there gave few hitechs benefit, and clearly – those supports were offered to companies that did not have the potential to scale up.

Very often, American Hi-tech companies and our Investment Bankers, became the primary benefactors of these accelerators, as a handful of break-out Canadian companies were spirited away by well intentioned leads at Canadian offices of Google, Microsoft, and others. Once a Canadian company was purchased however, it was no longer a Canadian Company, and, I think, most products, IP, and Canadian Hitech Jobs have been removed from Canada along with.

The Investment Bankers may have been happy to report an “EXIT”, but “POOF” went our chances at building a multi-billion-dollar company simultaneously.

And those were the lucky ones. HiTech startups, especially the robotic kind that can automate exports and self-sufficient assembly lines, need a program of reliable bridge(s) between “Funded Operating Windows”. Many entrepreneurs begin companies with family loans, or bootstrap their creations with personal savings, but these funds will run out – reliably.

Without an Engineering Safety Net, most entrepreneurs will not be able to afford to raise their families inside of housing bubbles – from their savings alone – and most will have to forfeit their dream of building a successful hitech.

Not one program is offered by any accelerator nor innovation nor research group in Canada, to provide basic salaries and offices so that companies can take a skeleton crew on to their next funding window. Not One; not in Ten Years of year-over-year failure to produce major Canadian HiTechs.

This is an easy problem to fix – and at the risk of being completely obvious, here it is: When support programs don’t work according to industry KPI measures, change up the supports. If no changes are made and results hold steady, replace the staff assigned with qualified hitech leaders. Finally, stop funding the accelerator and build different programs – and – figure out all of this not in ten years; but in two or three. For ten years, an entire startup career, Canada shows no sign of changing its losing Accelerator formula.

Incompetence – I mean that’s it isn’t it. No journalist likes to resort to insult and I mean none by stating a disappointing fact; that our government leadership team, alongside elected politicians and voters, are either afraid to change status-quo that empirically doesn’t work – or they are simply ignorant of their failings. And who can argue actual results …

Our economy did not get where it is, based on the strength of Canadian thought-leadership, so let’s add this Engineering Safety Net Policy to our turnaround plan. Policy that prevents candidates from political party’s that have not signed on to a long-term Strategic Right Plan, created by experts, is 20-years overdue as well – but I digress.

Major Financial Institutions – Failed Innovation

Now that we have bridges, on next to the problem of creating funded windows.

Major funds like the Canada Pension Fund or the Teachers Pension (two of the top-thirty funds in the world) – ensure that pension holders will have incomes that keep up with “normal” inflation rates, but I’ve already mentioned that there is little that is normal about our inflation this past 20-years – and most Fund CEOs worry about meeting their inflation mitigation targets during their public interviews and video’d presentations.

Investment Committees at these Fund Companies ensure that staff fund managers can seek out larger returns by setting aside a percentage of their monthly subscriber fees for investment in higher-risk public stocks, private companies, projects, real estate, and so on.

Professional financial analysts must Mitigate the Higher Risks presented in a sustainable way, but no requirement was ever made by our Government that they invest a percentage into Canadian Innovation companies.

Risk Mitigation – “the Blades of Grass” Detail

Adding social goals to major fund company investment is not enough, as we must work our way right down to the Risk Mitigation strategies that have prevented Canadian Startups this past ten-years.

Some Risk Mitigation strategies are sustainable; they create both strong, consistent returns – and they create strong economies. Unfortunately, however, the most widely approved approach in Canada is much more tactical than strategic.

Multi-year Track Record Strategy

In Canada, Fund Analysts protect their investment portfolios by looking for mature, pre-IPO companies that can easily prove several years of financial and production targets are met. This is regarded as a very easy investment to defend – and no analyst wants to risk his job and career over less-easily defended risk mitigations than this – if at all possible.

In the rapidly emerging robotics field however, this wait-and-see approach creates a chicken-and-egg shortage of available Canadian companies, it denies us the easy low-hanging-fruit IP (Intellectual Product/Patent Incomes) – there only for early entrants, and it denies the Canadian people GDP Export Revenues from the trade of our engineered robotics products.

Unfortunately, this is the only Risk Mitigation Strategy that permits the Analyst to keep his job, by the rules of the Investment Committee – so he’s good – at least until the economy around him (or her) collapses and he cannot get to work because his kids cannot attend unsafe schools alone – or his plush home is lost to rioters; you get my point.

I tried to create an autonomous driving fund with Canadian Companies several months ago. We literally have none. One advancing Waterloo startup was just beginning to talk about this, but no opportunity at investment exists in Canada because there are no companies here. You need a chickens to harvest eggs; you need companies to attract international hitech investment. Canada has the smart engineers; but we don’t have the companies.

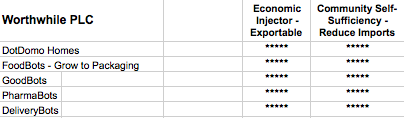

A too-conservative approach – in Robotics specifically, creates a significant sustainability issue for economies as mentioned above. Worthwhile Ventures’ Robotics rate their Smart City economic contributions in charts to make the sustainability benefit clear:

Although a Fund Manager, Pension Fund, etc., might seem to succeed by investing in mature foreign companies initially, the resulting economic and social collapses that must follow the accelerating trade-deficits created, make this strategy unsustainable.

Canada is a rare country, to not need barred windows and gated communities; to have safe schools, etc. – but this will change with economic collapse and with inequity’s undermining impact upon our democracy.

The “Multi-year Track Record” Risk Mitigation Approach for Innovation is unsustainable just as is any Financial Sector Investment Processes which prospers while failing to monitor and safeguard the health of host country economies.

Smart-Revenue Ramp-up Approach

Smart-Revenue Ramp-Up Approaches greatly reduce Risk – and they also greatly reduce Return on Investment (ROI) Timelines.

Automation Products can take from twelve to eighteen months to develop. If we build a business model for this R&D Product Development in isolation, we have no products to sell until a complex design and build project is complete. At the time that the prototype and product are tested and ready for market, we must spend again in support of sales and marketing of the product. Only at this time, can we hope to create revenues from the sale of Robotic tools – and decision windows for Robotic sales can be quite steep owing to their high cost. This strategy creates a very long ROI recovery timeline that is often unattractive to investors who realize that the developed tool(s) might not be popular as a new market entry for several years as well.

A Smart-Revenue Ramp-Up Approach develops Commodity Products Manually and Robotic Automation Products. This reduces Risk in three ways:

- It improves a company’s understanding of the processes needed to automate a full solution

- It generates revenue immediately, which offsets the expense of the automation teams during their least profitable R&D work; reducing ROI dramatically.

- We eliminate the chicken-and-egg problem created by relying on a Multi-year Track Record Approach for Risk Mitigation. This means that a country can beef up production of automation in support of their Exports and Self-Sufficiency

At a point, the robotic productions outpace manual productions and those workers can now move into other roles, training, etc. – with incomes protected by #TEMature Government Support Policy described above.

By monitoring Smart Revenue Ramp-up targets carefully, we eliminate Risk to targets and to the economy.

Local companies can now begin to contribute to export and economic self-sufficiency robotically, while meeting targets reliably. And, this is just one example of a sustainable solution to HiTech Risk Mitigation. There are others…

Where we are

Investment Committees at major Funds are not yet insisting on correction from their Due-Diligence teams. This should change, as alternatives like “Smart Revenue Ramp-Up Approach”, serve sustainable-investment needs better short, mid, and long term.

Noted Oxford Press author Stephen Pressfield, in his landmark book War of Art, would refer to this Smart Revenue Ramp-up as a Professional’s approach to Risk Management.

-

AuthorPosts

- You must be logged in to reply to this topic.